Macro roundup: Duelling accounts

Greece's statistics bodies release a wealth of sectoral data

Programming note: Grecology is on vacation and will be off for a couple of weeks. The next weekly roundup will come out on Aug. 18.

This week saw the release of two of my favourite data sets — the sectoral non-financial accounts from the Hellenic Statistical Authority and financial accounts from the Bank of Greece.

These accounts are highly complementary in theory, since they both arrive at net borrowing/lending positions for each sector. Unfortunately, as we noted last week, there is a large statistical discrepancy between the two, which has the effect that I use the central bank’s data (also known as the flow-of-funds) much less that I would like.1

For example, the central bank’s financial accounts consistently estimate a better net lending/borrowing positions for Greek households than the statistical authority, Elstat, does. In fact, the flow-of-funds data suggests that they have tended to be net savers since the country’s adoption of the euro, whereas Elstat’s data shows that they have been net borrowers for all but a few quarters after the pandemic’s outbreak.

All of which is to say that the flow-of-funds data need to be treated with some caution. Nevertheless, it's a fascinating dataset since it shows what financial assets and liabilities each sector is accumulating against each other sector.

For instance, Greek households decreased their overall cash and deposit holdings in the first quarter by 3.01 billion euros.2

We’ve known for a while about the drop in deposits from the central bank’s monthly deposit data, which also show that there has been a rotation out of sight deposits and into time deposits. This is because interest rates have increased slightly on the latter, while they remain close to zero on the former.

At the same time, the flow-of-funds data shows that households’ search for yield also led them to increase their holdings of government treasury bills by 609 million euros, following a 198 million-euro increase in the fourth quarter of last year. Households also increased their holdings of foreign debt securities by 384 million euros.

The flow-of-funds data also show that the non-financial private sector as a whole got very close to achieving a positive financial net worth for the first time in almost a decade in the fourth quarter, but dipped slightly in the first quarter.

The Greek private sector’s financial assets increased in the first quarter — mostly as a result of higher valuations of unlisted shares and other equity. However, on the liability side, the value of the holdings of unlisted shares and other equity in Greece by overseas residents increased even more.

Wage gains

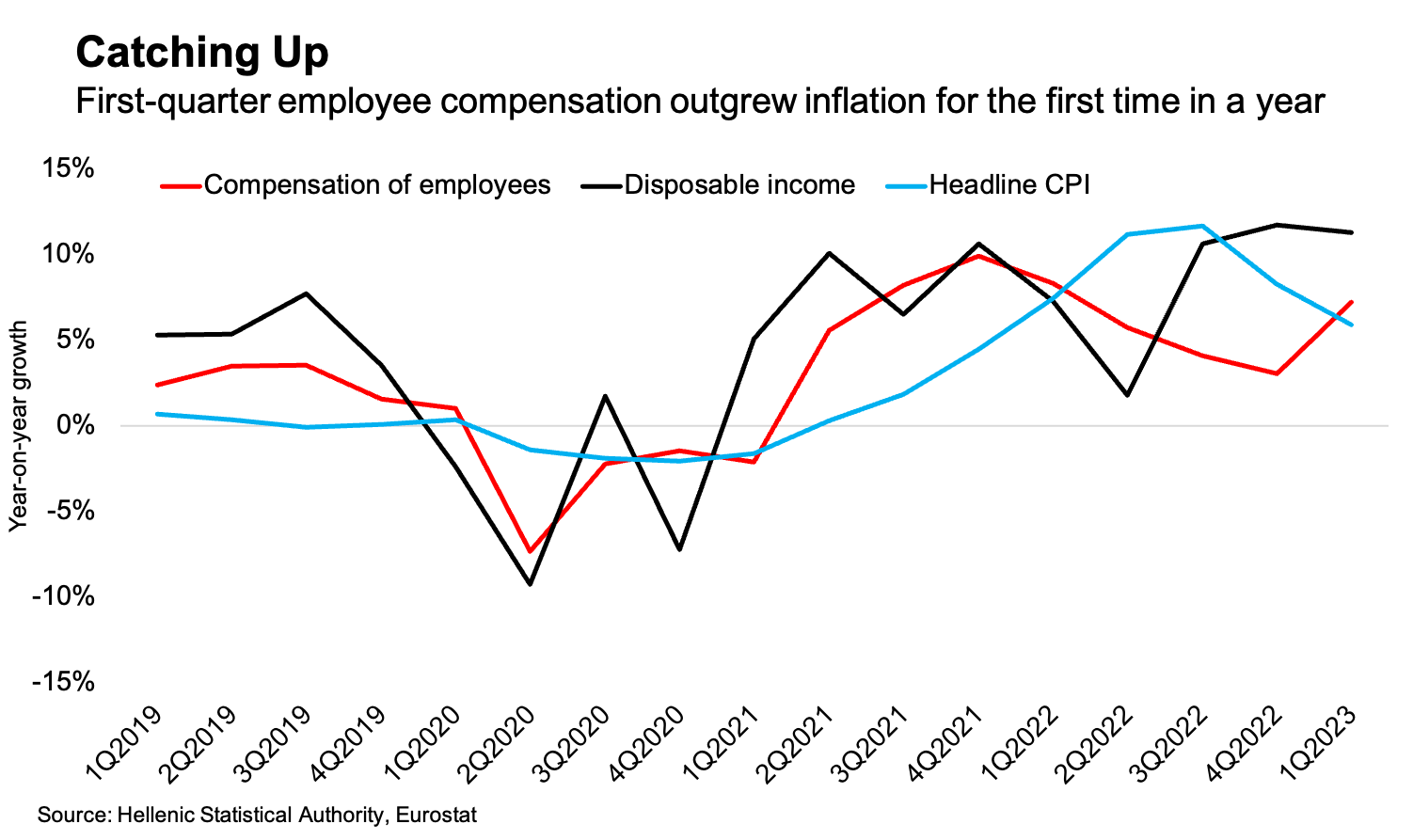

Turning now to Elstat’s non-financial sectoral accounts, one highlight was the strong growth in employee compensation in the first quarter, which increased by 7.2 percent from a year earlier, compared with 3 percent in the last quarter of 2022.

Taking transfers and other income into account as well, household disposable income grew 11.3 percent in the first quarter, compared with 11.7 percent in previous quarter.

We noted a few months ago that after adjusting for inflation, Greeks’ disposable income decreased in 2022. However, inflation is now on a downward trajectory — not withstanding the continuing growth in food prices — and disposable income growth has outstripped the growing cost of living for two straight quarters. Added to that, the growth in employee compensation also higher than headline inflation in the first quarter for the first time in a year.

On a final point from the sectoral accounts, the flip side of social transfers boosting disposable income as that there was a slight deterioration in the government’s fiscal balance in the first quarter compared with the same quarter of 2022 — with the main cause of this being an increase in social benefits.

With elections taking place in the middle of the year, the government spent quite liberally on social programs at the start of the year — and this will leave the government finances playing catch-up for the rest of the year.

Credit tightening

The growth rate of Greek bank lending to the private sector slowed to 2.8 percent in June from 3.1 percent the month before and from a recent peak of 6.3 percent at the end of 2022.

For non-financial corporations, the growth rate slowed to 5.8 percent from 6.7 percent in May and 11.8 percent in December. Consumer credit growth increased slightly, although overall lending to households shrank 2.7 percent, compared with a 2.8 percent contraction the month before.

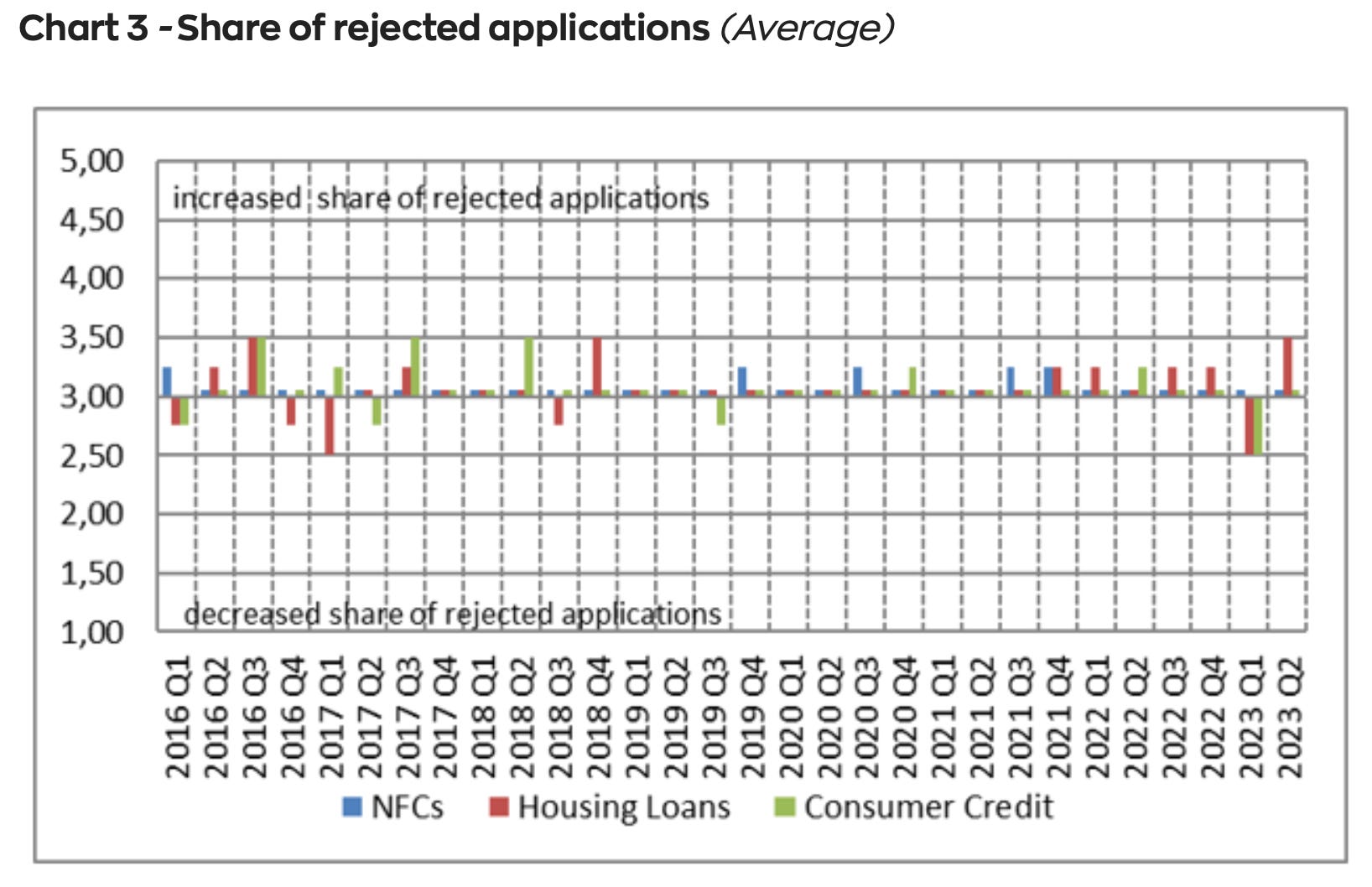

Meanwhile, the Bank of Greece also released the bank lending survey for the second quarter, which showed an increase in demand for business, consumer and housing loans. The increase in demand for housing loans was especially pronounced.

We’ve talked quite a bit recently about the booming housing market, and this suggests people are getting more desperate to get on the ladder before prices go up even more. However, as we’ve also noted, mortgage lending has continued at a steady contractionary pace for more than a decade and has played little role in the current housing cycle.

As they invariably do, loan officers surveyed by the central bank report no easing or tightening in credit standards in any of the aforementioned categories.

Nevertheless, the counterpart to the increase in demand for mortgages has been an increase in the share of rejected applications.

Other data

The number of visitors to Greece in the first five months of the year increased 32.9 percent from a year earlier to 5.76 million people.

Travel receipts increased 30.7 percent to 3.24 billion euros between January and May.

The average spend per visitor was 541 euros, down from 554 euros in the same period of 2022.

Private sector deposits held at Greek banks increased 3.01 billion euros in June to 189.3 billion euros — the largest monthly increase so far this year.

Deposits held by households increased 941 million euros, while those held by non-financial corporations increased 2.43 billion euros.

The economic sentiment indicator for Greece improved to 111.1 in July from 110.1 the month before.

It marks a further divergence from the average for the euro area, which deteriorated for a seventh straight month in July.

Greek consumer confidence also improved.

Building activity, as measured by the number of permits issued, increased 0.9 percent in April from a year earlier.

The number of permits issued in the first four months of the year increased 10.1 percent from a year earlier.

Greece’s producer price index decreased 11.7 percent in June from a year earlier, compared with a decline of 12.9 percent in May.

Next two weeks’ key releases

Monday, July 31:

May retail sales (Elstat)

Tuesday, Aug. 1:

June labour force survey (Elstat)

July manufacturing purchasing managers’ index (S&P Global)

Tuesday, Aug. 8:

July consumer price index (Elstat)

Thursday, Aug. 10:

June industrial production (Elstat)

Elstat’s national accounts data takes precedence because it is part of the same system of national accounts that also measures gross domestic product and government finance statistics. It also gives a net position for the rest of the world that has a smaller statistical discrepancy with the balance of payments data than the flow-of-funds does — even though the latter two datasets are both produced by the Bank of Greece.

If I were to guess, I imagine that cash holdings associated with the grey economy lie at the root of the large statistical discrepancy.