Navigating turbulent economic times

My own grading of Greece's economic performance under the current government

Greece is a small country buffeted by economic winds it doesn’t control. So when assessing its macroeconomic performance under the current government — or any government over a four-year period — it’s important to acknowledge that much of what we see is down to the happenstance where the country happens to be in the business cycle, external shocks and policy decisions made far away from Athens.

Earlier this week, we hosted a guest post by Dimitris Valatsas, who writes the Macro Letter, grading the government’s macroeconomic performance. I found Dimitris’s analysis excellent and eye-opening, but I didn’t agree with all of the marks awarded.

In justifying my own grading, I will follow the same framework that Dimitris sets out. In his words:

“I focus here on five distinct areas: gross domestic product, the labor market, real wages, investment, and inequality. I am deliberately avoiding any discussion of the deficit and the public debt load — in part because this issue receives ample attention as it is and in part because Greek debt dynamics are very peculiar. I am also avoiding any direct judgment on inflation (other than through real wages) given that exogenous inflation is beyond the government’s control, while endogenous inflation is primarily an issue for the European Central Bank.”

I completely agree with Dimitris that the government shouldn’t be judged on inflation. In fact, I always thought the political criticism on this issue was wide of the mark. The inflationary pressure Greece has faced is a prime example of a macroeconomic gust it can’t control.

In fact, I would extend this principle.

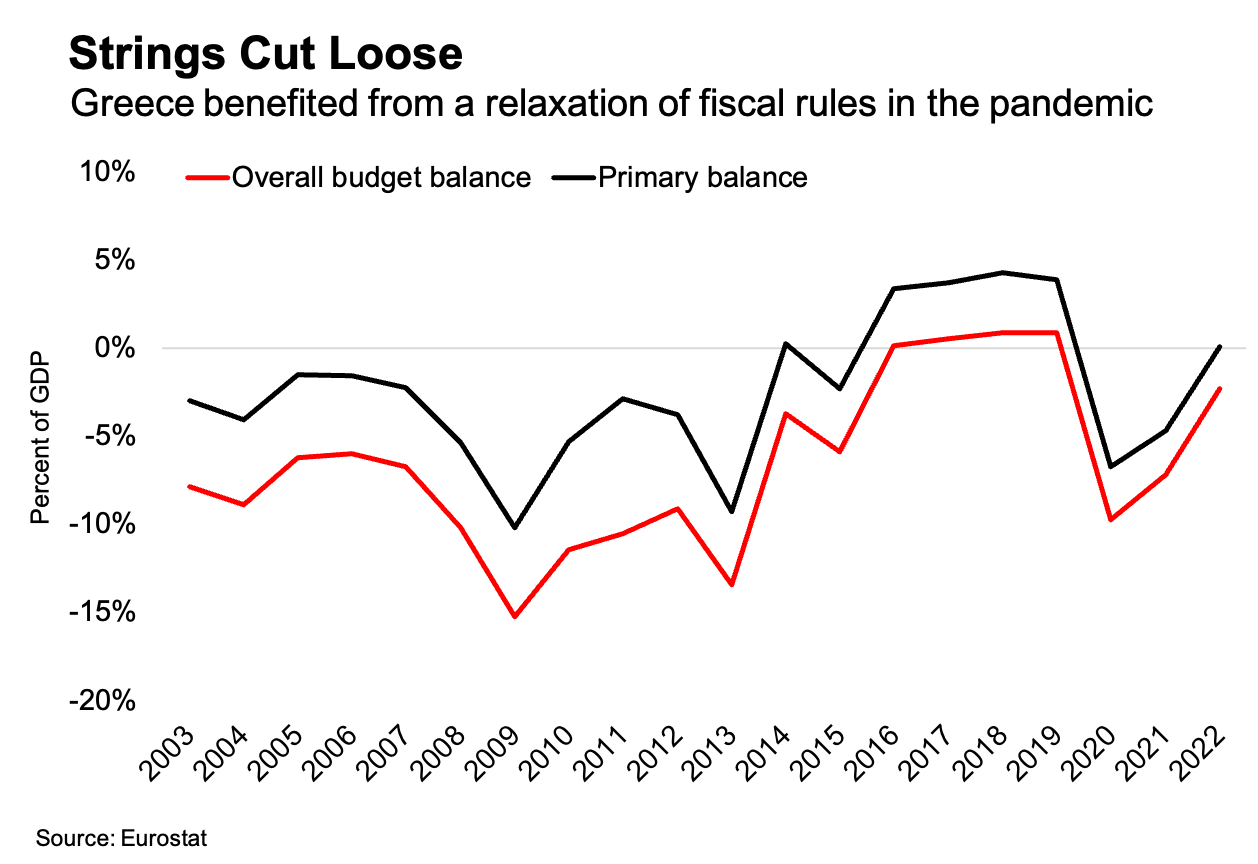

Economic winds beyond the government’s control have also filled its sails. Having learnt some lessons from the euro crisis, when the pandemic struck the euro area suspended fiscal rules that bound previous administrations. That in turn meant the government had permission to run a counter-cyclical fiscal policy, which has been a critical driver of Greece’s economic performance during this period.

This isn’t to say that I think the government is a helpless victim of circumstance and can’t receive any praise or criticism at all. The most obvious way governments in Greece can have a big impact on macroeconomic developments is by screwing things up. Low-key competent macroeconomic management is nothing to sniff at.

Rather, I think the bar for handing out “A’s” when it comes to the economy’s performance needs to be high. Especially if we choose not to judge the government over inflation hitting double digits. So I will go through the five areas Dimitris outlines and offer my own grades.

Before that, a caveat: Grecology is a newsletter that generally focusses quite narrowly on macroeconomic developments. There are more issues at stake on Sunday, including national security, human rights, migration, healthcare, education and many other things. Economics is what I write about, so that is what I focus on here, but this is not an overall judgment on the government.

GDP: much needed recovery momentum

Dimitris gives the government an “A” for the 5.7 percent cumulative increase in gross domestic product that took place between the second quarter of 2019 and the end of last year, a period when the euro-area average growth was 2.4 percent.

The arc of this period is output falling dramatically for all euro area countries in 2020 due to the pandemic, before rebounding sharply thereafter. Since all euro-area countries shared the same policy environment, Greece’s GDP performance relative to its peers can be seen as a proxy comparing its handling of economic conditions.

It’s great news that Greece’s economy is growing so much faster than the euro-area average rate, but it’s also what you would expect should happen. When Mitsotakis came to power, the country was just coming out of a “lost decade”, an economic depression that wiped out a quarter of its GDP. When the recovery began in earnest, it was always likely to be supercharged by rebound growth and abundant spare capacity.

The chart above compares output gaps — the difference between actual and potential GDP, as a proportion of potential GDP — for euro area countries at the end of 2018 and at the end of last year, as estimated by the European Commission. These figures need to be treated with extreme caution for reasons that we don’t need to expound on here.1 But for our purposes, they serve as an illustration of the different starting points between Greece and the rest of the euro area during our reference period.

There’s also the underlying structural issue that sustained GDP growth is causing the current account deficit to grow alarmingly. Last year it widened to 8.2 percent of GDP from 4.5 percent the year before — a shift that was solely down to rising energy prices.

This is a deep cause of worry, and something that I’ll look at in more depth in a future post. For now, I’ll give the government a pass because Greece’s structural economic pathologies are things that will take several government and several terms to put right.

Nevertheless, I’m going to keep Dimitris’s “A” here because I’m not sure what more it would be reasonable to expect in terms of GDP growth. But in awarding the highest grade, we’re using up the government’s not-screwing-things-up credit. So it raises the bar elsewhere — especially when we grade employment and investment, since growth in both these areas is function of GDP growth.

Employment: More economic activity creates more jobs

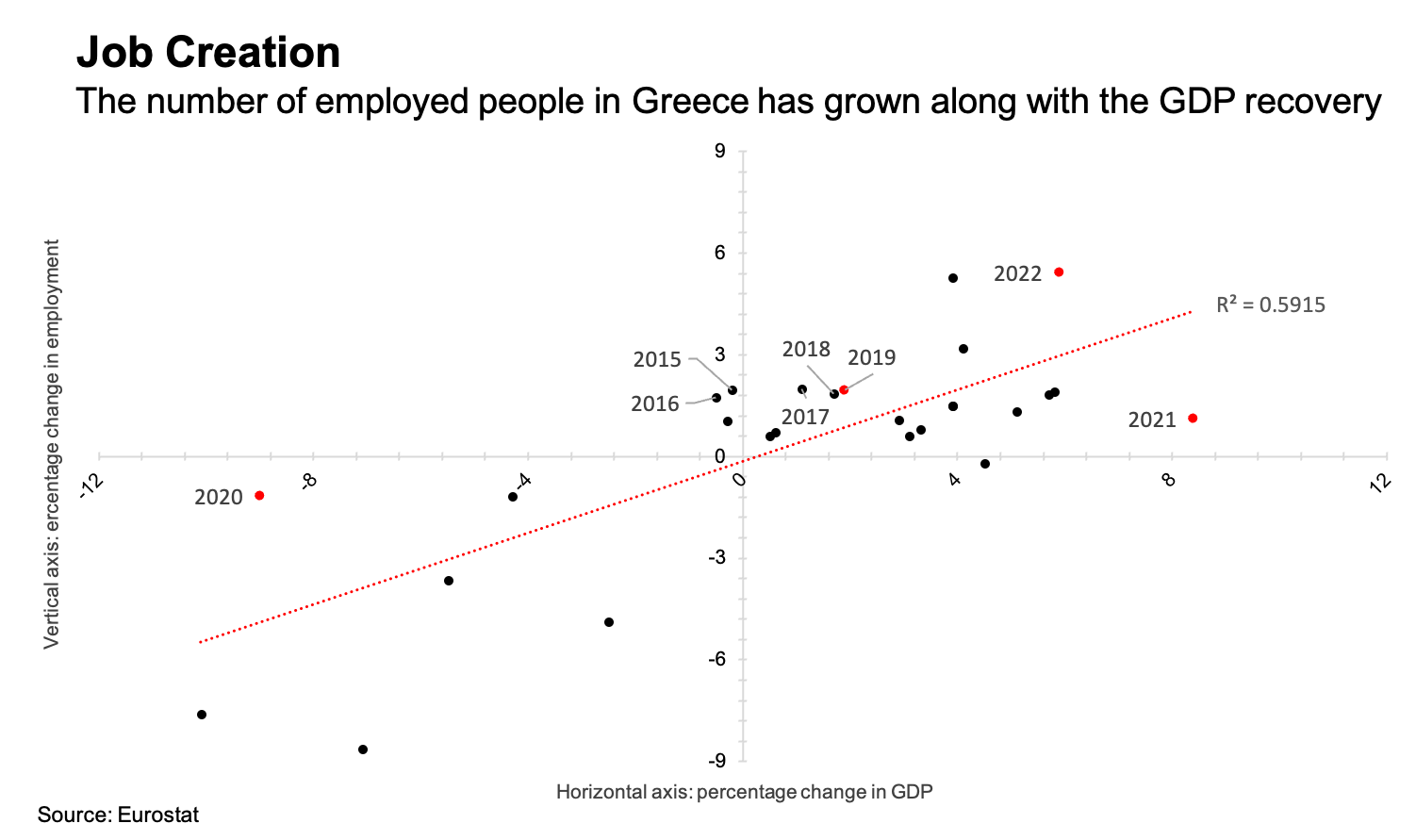

Dimitris compares employment gains in Greece with the rest of the euro area. As with GDP, the starting points are very different though. Greece’s unemployment rate peaked at in 2013 at over 28 percent, and it was still at 17.6 percent in July 2019, the month the current government took power. That’s a lot of spare capacity in the economy, and it left a lot of low-hanging fruit in terms of new-job creation.

The chart above plots the annual change in GDP against the annual change in employment for years going back to 1996. Last year does stand out as a strong year, but taking the last four years as a whole, it seems broadly in line with what we would expect for new jobs given this level of GDP growth.

Since we’ve already rewarded the government with the top grade for GDP growth, I’m going to give the “B” for employment, instead of the “A” that Dimitris gives. I think there’s a case to make for reversing those grades, but not a strong enough case for awarding an “A” in each.

Real wage growth: really poor

Here’s some of what Dimitris has to say in the section on real wage growth:

“Real compensation of all employees has increased since the end of 2018 (I’m using the annual Eurostat dataset), by 1.75 percent. This is below the Eurozone average of 2 percent over the same period. However, this concerns total compensation — as we saw above, the number of Greeks employed has grown by about 9 percent over the same period. Assuming the data is directly comparable, this translates into a purchasing power loss of 7.25 percent per working Greek — a woeful performance.”

I don’t think there is much that I can add to Dimitris’s excellent analysis in this section. But I struggle to see a 7.25 percent loss of purchasing power per working Greek as being worthy of a “C”. This one is a “D” for me.

Investment: an encouraging start, but only a start

As Dimitris points out, investment was in a state of collapse when Mitsotakis’s New Democracy party took power in 2019. So while the growth in gross fixed capital formation since 2008 is impressive — 32 percent in real terms, 42 percent in nominal terms — these figures are so striking because the denominator is so low.

As an illustration of just how dreadful Greece’s levels of investment remain, gross fixed capital formation is still lower than consumption of fixed capital, or depreciation. So the stock of fixed capital has actually decreased under this administration.

Aside from the data contained in the national accounts, there are other encouraging signs. Foreign direct investment into Greece last year hit a record — although a large part of this is either real estate or M&A activity rather than greenfield investments — and there’s been positive news flow about new projects approved and signed with funds from the European Union’s Recovery and Resilience Facility.

Those signs make me hopeful that if we’re doing this exercise again before elections in 2027, then I will be able to award the government of the day the top mark for investment. Now, since we’re grading what has happened in the last four years rather than what might happen in the next, I’m going to revise Dimitris’s “A” down to a “B”.

Inequality: stalling progress

As with real wage growth, I don’t have a lot to add to Dimitris’s analysis of the data in this area. Initially I struggled to reconcile that analysis with the “B” that he awards. The analysis shows that Greece made big progress in reducing inequality in the years before 2019, then that progress stalled. For me, that looked more like a “C” at best.

Policy choices were involved here. The previous government oversaw the improvement we see in Dimitris’s analysis while carrying out a fiscal consolidation of about 3.5 percent of GDP. It made choices concerning taxes, social security contributions and pensions that were criticised by both the International Monetary Fund, and by Mitsotakis when he was in opposition.

This often gets framed as a tradeoff between growth and inequality, or as a choice between policies that focus on cutting the pie more evenly versus policies that grow the pie. This is an analogy that’s Mitsotakis himself likes to make.

So how much has the pie grown under the current government?

We’ve already discussed GDP, but perhaps more relevant here is household disposable income. Taking a four month moving average of the quarterly data (to adjust for seasonal variation), this grew by 14.1 percent in nominal terms between the second quarter of 2019 and the last quarter of 2022. But most of those gains are eroded by inflation — adjusting for that, the increase becomes a much more modest 3 percent.

That said, this is one area where I’ve changed my mind in the course of writing this post and looking at the data, and I will keep Dimitris’s “B”. This is because I want to be consistent, and having stated that I don’t think the government should be judged on the high inflation we’re seeing, the corollary of that is that we shouldn’t be blame it for the rising cost of living reducing the purchasing power of disposable income.

Also, this disposable income would be even less if not for the transfers and subsidies that the government carried out to counter first the pandemic, then the rising cost of living. So although I come away wondering if I’m being too generous, but I will give the government the benefit of the doubt.

Summary: Cyclical upswing, risks ahead

Rereading Dimitris’s summary, there isn’t anything that I disagree with. Overall, I think the government’s handling of the economy has been reasonably good. If you aggregate the scores, Dimitris gives the government a grade point average of 3.4, which translates to a “B+”, while I will give them a GPA of 2.8, which is somewhere between a “B” and a “B-”. The difference between us isn’t great.

When the current government came to power in 2019, my feeling at the time was that the Greek economy was in a sweet spot of the business cycle where it was poised for several years of strong growth. Greece had exited its bailout programme the year before, no additional fiscal tightening was required and a change in government would kindle the “animal spirits” in business decisions that would catalyse a period of rapid recovery growth.

We’ll never know how things would have panned out if the pandemic hadn’t intervened so soon after. However, most of those factors remained in place, or even became more favourable — notably, the government could use fiscal stimulus to get the economy going, while the RRF was added to the toolkit to focus investment. Against that, inflation reared its head, presenting other kinds of challenges.

On net, I think these forces have presented opportunities and helped the government achieve that period of rapid growth that seemed in the offing when it took office.

There is, however, one thing that we have only touched on briefly, and that is the external sector. Greece’s true Achilles heel is its reliance on forbearance from the rest of the world to finance its persistent current account deficits.

The Finance Ministry’s own projections show net borrowing from the rest of the world only coming down to 5 percent by 2026. The ministry projects that its government budget will be almost balanced that year, so the deficit with rest of the world corresponds to growing indebtedness of the private sector.

Exploring this aspect further requires its own post, and it goes beyond the framework we’ve set here. But typically, that’s a pattern that’s associated with growing financial fragility. It also highlights the dangers of handing out grades on the basis of on incomplete business cycles. Let’s hope investment and longer-term changes to Greece’s structural model resolves these imbalances.

A few years ago the economist Robin Brooks launched a social media campaign against “nonsense output gaps”, which drew some attention to the problem of estimating output gaps using tools like Kalman filters, which are essentially just glorified trend lines. These can underestimate potential output in a country that has gone through a sustained period of slow growth. A manifestation of this in the chart above is that Italy is shown running above potential output in 2018, which is patently absurd. This criticism is correct, in my view, but I don’t think it much matters for the limited point we are making.