Macro roundup: Outward resilience

The inflow of RRF funds is making its mark on Greece's external accounts

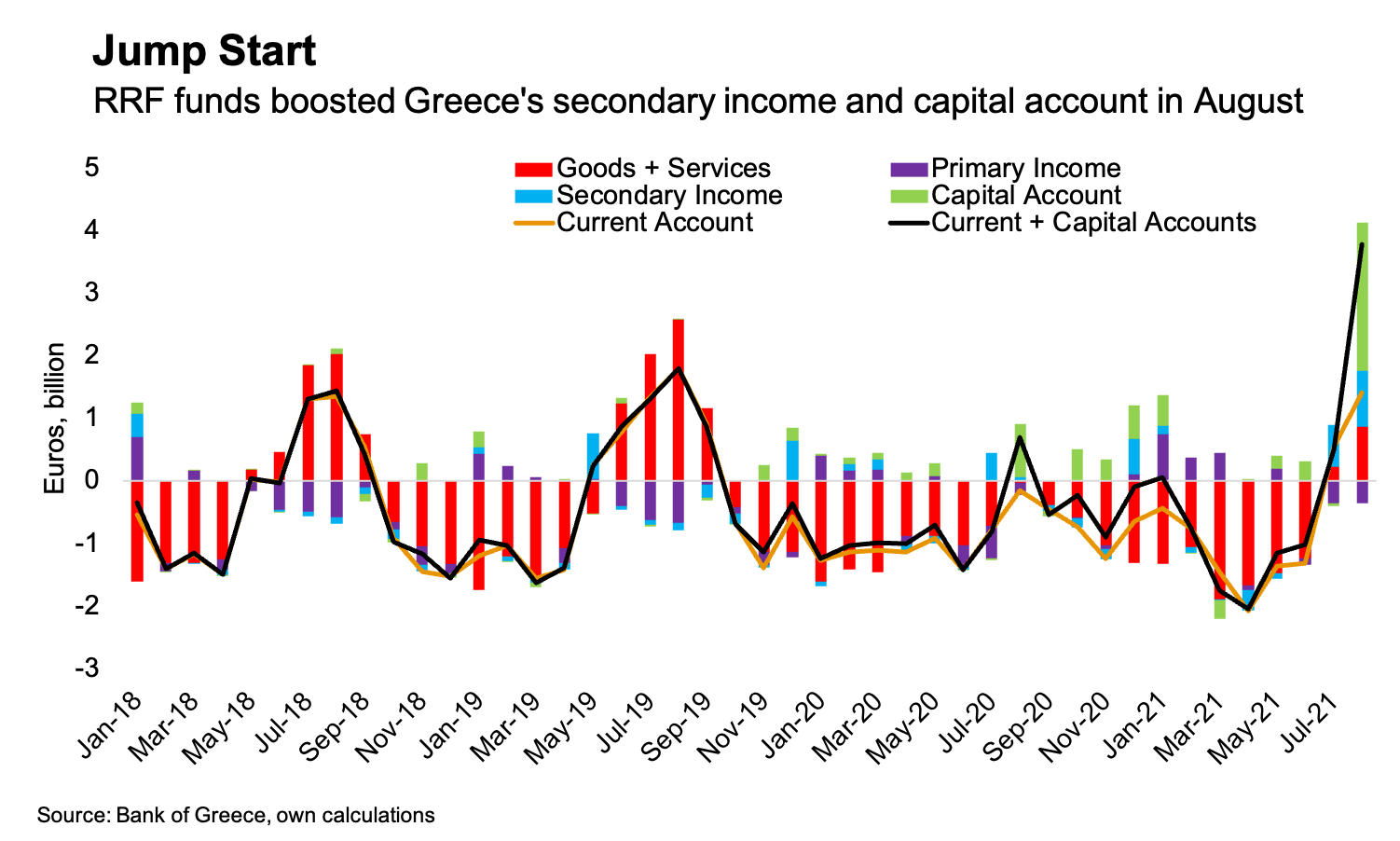

There’s a lot going on in the August balance of payments figures released this week.

The easiest thing to note is that the better-than-expected tourism season drove Greece to its biggest monthly current account surplus since before the pandemic. Travel receipts came to 3.11 billion euros — recovering to 75 percent of their August 2019 level.

The first arrival of funds from the Recovery and Resilience Facility also made an impact on the external accounts, and could be indicative of new trends. That impact included 2.3 billion euros in the capital account — which presumably mostly covers any projects with bricks and mortar, wheels or cables attached — and another 1.12 billion euros in the secondary income component of the current account.

Putting these elements together gave Greece a combined current and capital account surplus of 3.78 billion euros in August, the highest monthly total since 2013.

The counterpart of that (after subtracting 498 million euros for errors and omissions) was a 3.28 billion-euro surplus on the financial account. The infusion of RRF funds makes an impact here too, in the form of 1.66 billion euros of loans to the general government1.

New phase

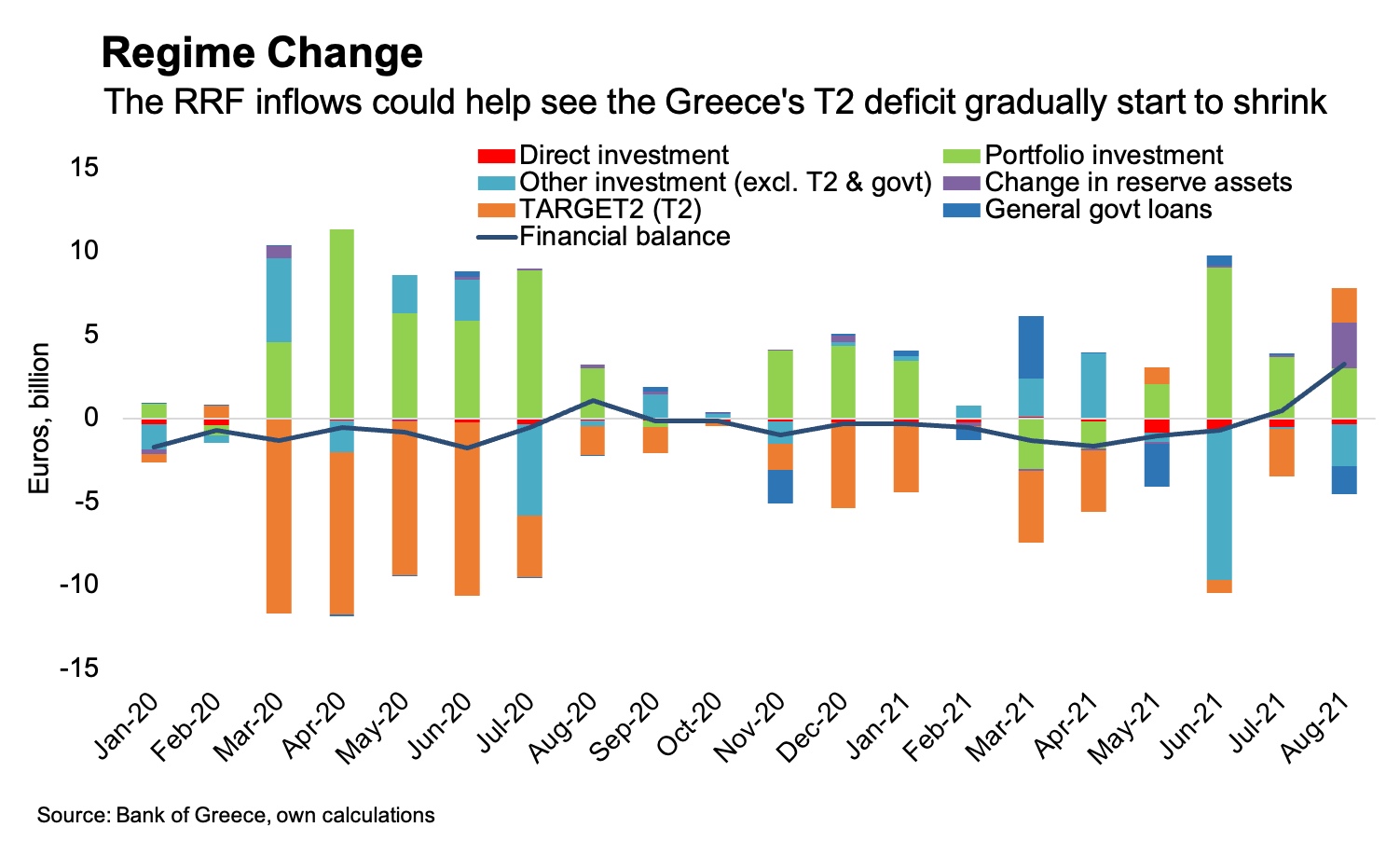

The reason why Greece managed to weather the economic crisis induced by the pandemic was because of the European Central Bank’s massive monetary expansion. A recurring theme of this newsletter is that the central bank’s TARGET2 accounts reveals the plumbing of the transmission mechanism for this expansion in Greece. That showed up as a rapid expansion of the TARGET2 deficit last year, before stabilising slightly this year.

But now the acute stage of the crisis is over and the economy is entering a new phase. We observed this last week with regards to the public finances, but it’s logical that we’ll see this in the external accounts too.

The TARGET2 deficit decreased by 2.02 billion euros in August.2 The TARGET2 balance doesn’t show up in the balance of payments itself, but rather in the financial sector balance sheets, released separately by the Bank of Greece. We have those figures for September, and they show the deficit falling another 875 million euros.

Overall, there are several one-off and seasonal factors that affected August’s balance of payments. However, as economic conditions normalise, there’s less stretching of the TARGET2 system to provide the elasticity for the financial system to operate without stress.

New patterns are likely to emerge in the financing of the current account deficit. RRF disbursements won’t be a monthly occurrence, but with north of 30 billion euros of funds earmarked for Greece under the programme, they will be an important part of the mix.

If you’re enjoying this newsletter, consider sharing it with others who might also like it.

Next week’s key data

Monday, Oct. 25:

January-September budget execution, final data (Finance Ministry)

Tuesday, Oct. 26:

Third quarter bank lending survey (Bank of Greece)

Wednesday, Oct. 27:

September bank lending and deposits (Bank of Greece)

Thursday, Oct. 28:

October economic sentiment (European Commission)

Friday, Oct. 29:

August retail sales (Elstat)

Elsewhere on the web

Nektaria Stamouli reports on the far-right resurgence in Greece.

The failure of Greek banks to lend more to the economy has been noted.

Matthew Klein on paying the Covid bill.

Farewell then, Jens Weidmann. Arsenal fans (and probably only Arsenal fans) will understand why it’s impossible for me to hear his name without mentally changing it to “Mad Jens Weidmann”. Yet when the chips were down with all that Karlsruhe nonsense last year, he fell into line — ducking his chance to be a true berserker like his goalkeeping namesake. Anyway, I’m no BuBa watcher, so here’s something from OMFIF on his departure.

Here’s another contribution to the Great Inflation Debate, from Jo Michell.

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.

Last week we noted the impact of the RRF funds on the central government budget execution, which amounted to 2.3 billion euros of revenue. That maps neatly onto the 2.3 billion euros recorded in the capital account, which added to the loans recorded in the financial account matches the 4 billion euros disbursement announced in August.

Chris Marsh, who blogs as the General Theorist, has made the point that changes in the T2 balance for Greece, given the euro-area’s architecture, are akin to changes in reserve assets. With that in mind, it’s ironic that Greece’s actual reserve assets — which don’t normally change much — also jumped by 2.76 billion euros in August, due to the International Monetary Fund’s new allocation of Special Drawing Rights.