Macro roundup: Mystery in the terms of trade

Against all intuition, Greece's terms of trade apparently improved in 2022

There was some good news from Greece’s balance of payments data for January, as the current account deficit for the month shrank to 125 million euros from a deficit of 2.12 billion euros in the same month of 2022.

This is encouraging since the explosive impact of the energy price shock on the country’s current account deficit was a cause for worry last year.

The January data show that exports of goods rose by 30.4 percent, while imports rose 5.6 percent. At constant prices, the increases were 12.3 percent and 1.2 percent respectively. This is the second straight month in which export growth outpaced imports, and is a reversal of the trend that prevailed for much of last year. Excluding oil, exports grew 4.2 percent at constant prices, while imports dropped 2 percent.

Strange terms

Meanwhile, the release earlier this month of national accounts data for 2022 gives us some more context for last year’s current account performance — and also throws up a mystery.

It’s usual to attribute the widening current account deficit to a deterioration of the terms of trade — which is the ratio between a country’s export and import prices. Given everything we know about what happened last year, with an energy shock that was exacerbated by Russia’s invasion of Ukraine, this is common sense.

The gross domestic product data gives us the deflators for imports and exports. These deflators — a measure of price changes — are used to calculate the terms of trade, which seemingly actually improved by 4.6 percent.

This result is not only counter-intuitive, but also stands in marked contrast with Greece’s eurozone peers, where you see the terms of trade deterioration that you would expect in 2022.

I’d be curious to know if there’s a good explanation for this result.

However, in a case like this, I suspect the error is more likely to lie with the data than with the intuition. As we’ve noted before, Greece’s GDP data is often subject to large revisions, so I wouldn’t be shocked to see this anomaly disappear after there have been a few more GDP releases.

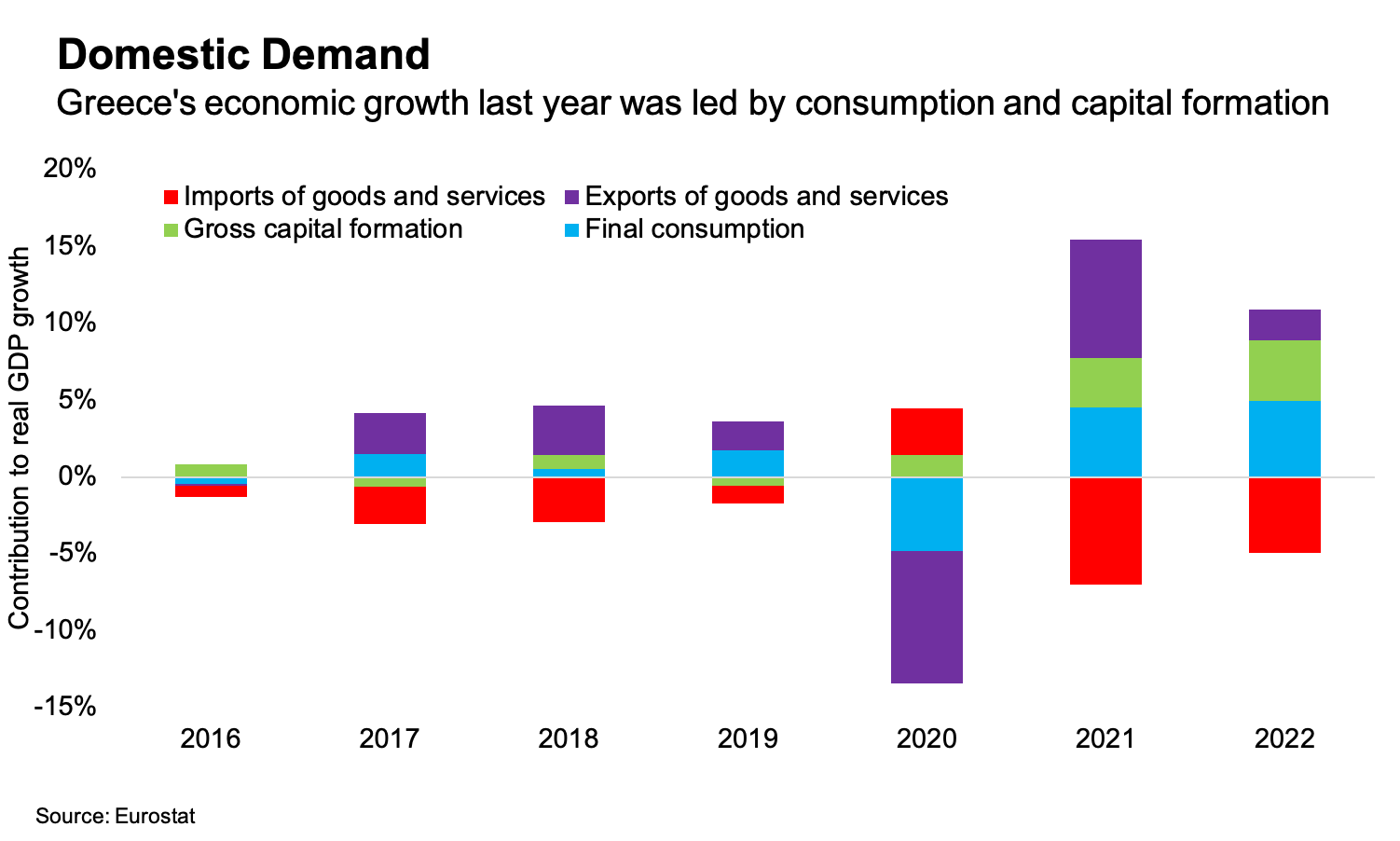

If we make the assumption that the terms of trade in 2022 were in fact worse than revealed in the national accounts data, that means that subtractive impact on GDP of the country’s trade deficit was smaller than revealed so far. This then implies one of two further possibilities: either real GDP growth last year was in fact higher than the 5.9 percent reported, or domestic demand (consumption plus investment) was weaker than initially reported.1

Other data

Apartment prices increased 12.2 percent in the fourth quarter from a year earlier, compared with 11.7 percent in the third quarter.

The average increase for 2022 was 11.1 percent, compared with 7.6 percent the year before.

In Athens, apartment prices increased 15.2 percent in the fourth quarter and 13 percent in 2022.

If you are enjoying this newsletter, then consider sharing Grecology with others.

Next week’s key releases

Monday, March 27:

February bank credit and deposits (Bank of Greece)

Jan-Feb central government budget execution, final (Finance Ministry)

Tuesday, March 28:

December building activity (Elstat)

Thursday, March 30:

March economic sentiment indicator (European Commission)

Friday, March 31:

February unemployment (Elstat)

January retail sales (Elstat)

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by replying to the email. If you’re not subscribed yet, consider doing so.

I have corrected this paragraph, after initially publishing it with the opposite conclusions – that weaker terms of trade would mean a greater subtractive impact of the trade deficit on GDP. I concluded that this would imply that either GDP growth was lower, or domestic demand was stronger. I got this the wrong way around.