Greece's economic tightrope act

The current account deficit exposes structural economic weaknesses

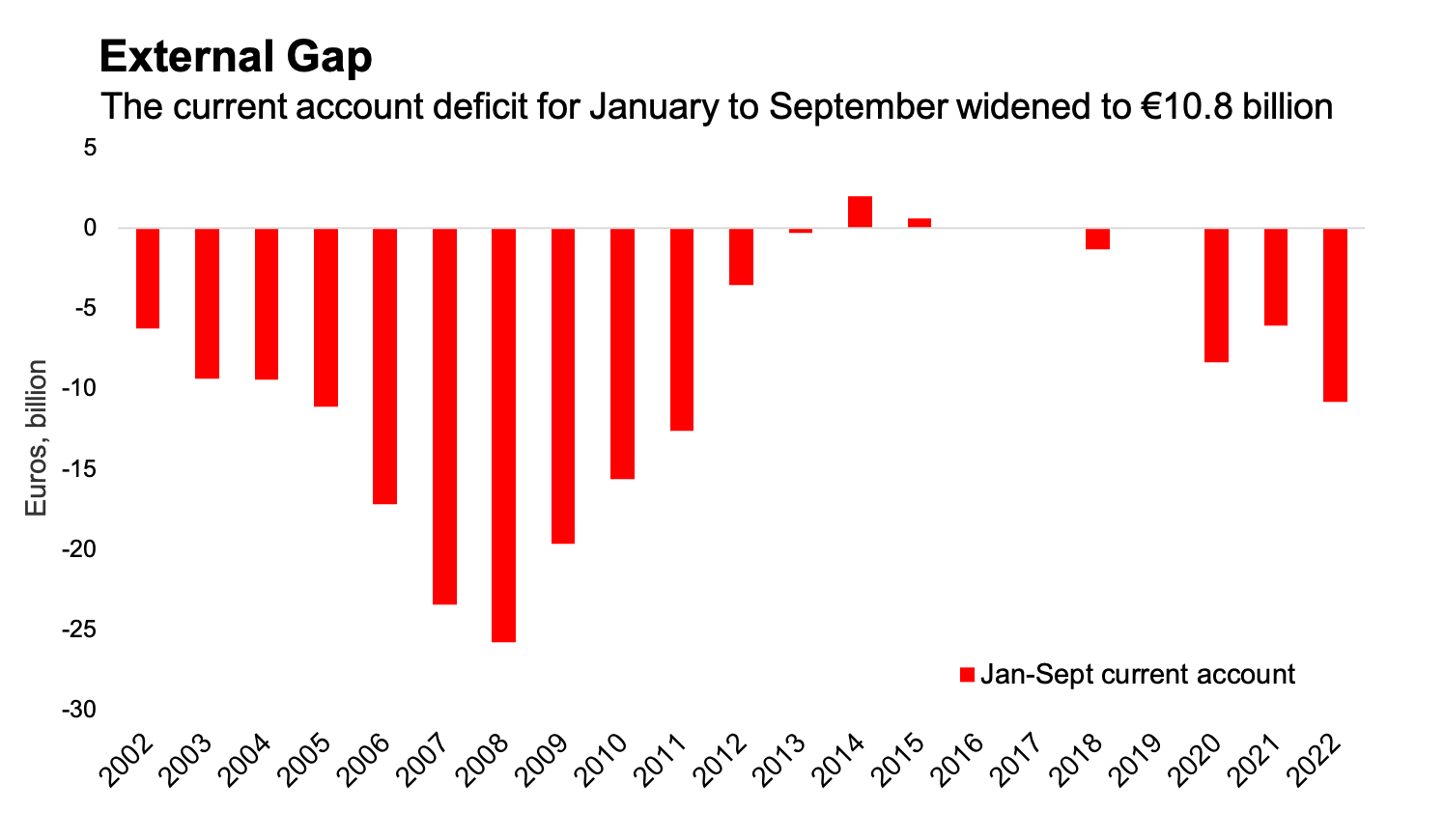

Beneath the main headlines about inflation and output growth, Greece’s current account deficit shows what a dangerous moment this is for the country.

The Bank of Greece’s balance of payments data for September, released this week, now encompasses all of this year’s peak tourism season. It confirms that travel receipts look close to matching their 2019 record. Despite this, the current account deficit overall looks set to exceed the pandemic-hit years of 2020 and 2021.

The deterioration in Greece’s external position was the unavoidable result of the sharp worsening of the country’s terms of trade given the energy and price shocks of the past year. Exports have performed well, even aside from tourism, but the effects of this have been drowned out by the rising value of imports, which grew by 47 percent in the first nine months of the year.

The price shocks have hopefully crested — and in terms of domestic consumer prices its encouraging that the inflation rate in October dropped to 9.1 percent from 12 percent in September. But while officials laud how tourism has helped Greece achieve one of the euro-area’s highest growth rates, the country’s current account deficit exposes the economy’s structural vulnerabilities.

Smashing it

Set against the worrying external picture, the public finances show a rosier picture, with the central government smashing budget targets set for this year.

The primary budget deficit for the first 10 months of the year came to just 349 million euros, according to Finance Ministry data. That compares with a 7.2 billion-euro deficit for the same period in 2021 and a target deficit of 6.7 billion euros.

While expenditure has also been lower than its target, the biggest driver of the budget over-performance has been tax receipts. These have been 5.1 billion euros higher than forecast in the 2022 budget.

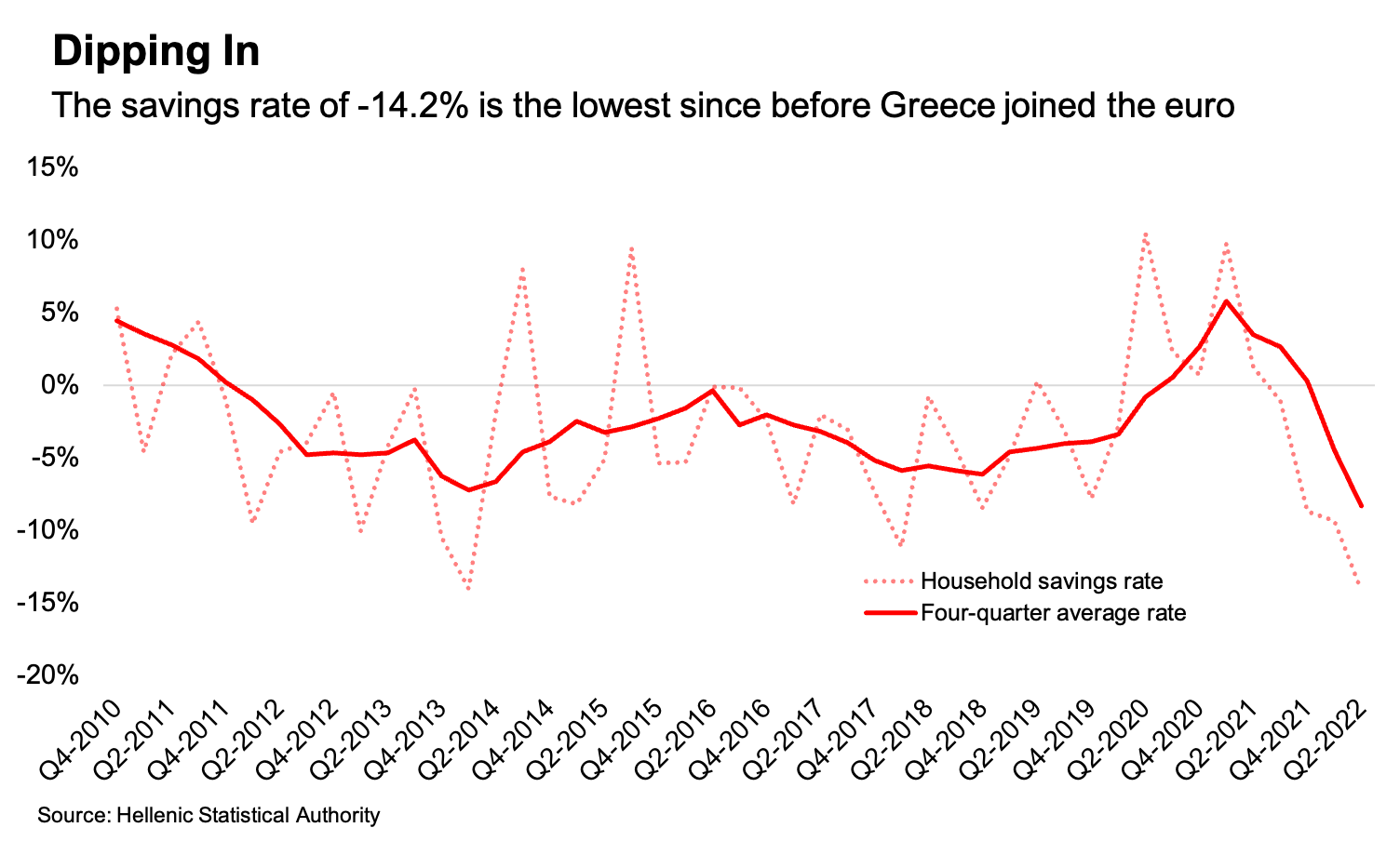

As a matter of accounting identity, when the government balance improves at the same time as the country’s external position deteriorates, that means that the private sector is increasing its indebtedness. That combination needs to be looked at cautiously as it is a common backdrop to heightening financial fragility and crises.

It is the case that banks, after disappointing drop off credit growth last year, have overseen a surge in lending to non-financial corporations in 2022, as well as a rise in consumer lending.

What we hope in these circumstances is that financing is being channeled toward productive investment that will transform the economy’s productive capacity and address its structural weaknesses. That’s certainly the official narrative, with funds currently flowing in through the European Union’s Recovery and Resilience Facility.

Little margin

The finance ministry this week submitted to parliament its draft budget for 2023, which forecast public and private investment rising to 15.5 percent of gross domestic product in 2023, an increase from 10 percent this year. The government predicts that RRF funds will next year contribute 1.9 percentage points to GDP growth, which it forecasts at 1.8 percent.

Beyond the near-term growth effects, only time will tell whether this investment will, at a microeconomic level, translate into something structurally transformative that diversifies Greece away from its reliance on tourism.

It feels paradoxical that for much of 2021 we were calling on banks to increase lending to Greece’s private sector in order to support economic growth — and now that we see that happening this year, we’re concerned about financial stability.

Nevertheless, that’s the world we live in. Greece is a small country with severe structural economic weaknesses, navigating through what the historian Adam Tooze has called a “polycrisis”. There’s little margin of error as a lot can go wrong.

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.