Credit Denied

Greek banks don't want to carry the can for weak lending growth

Some recent reports have suggested Greek banks really want to increase lending to businesses, but just aren’t finding enough demand. Companies are either using subsidised loans to refinance existing borrowing, or other government programmes are allowing them to meet their liquidity needs.

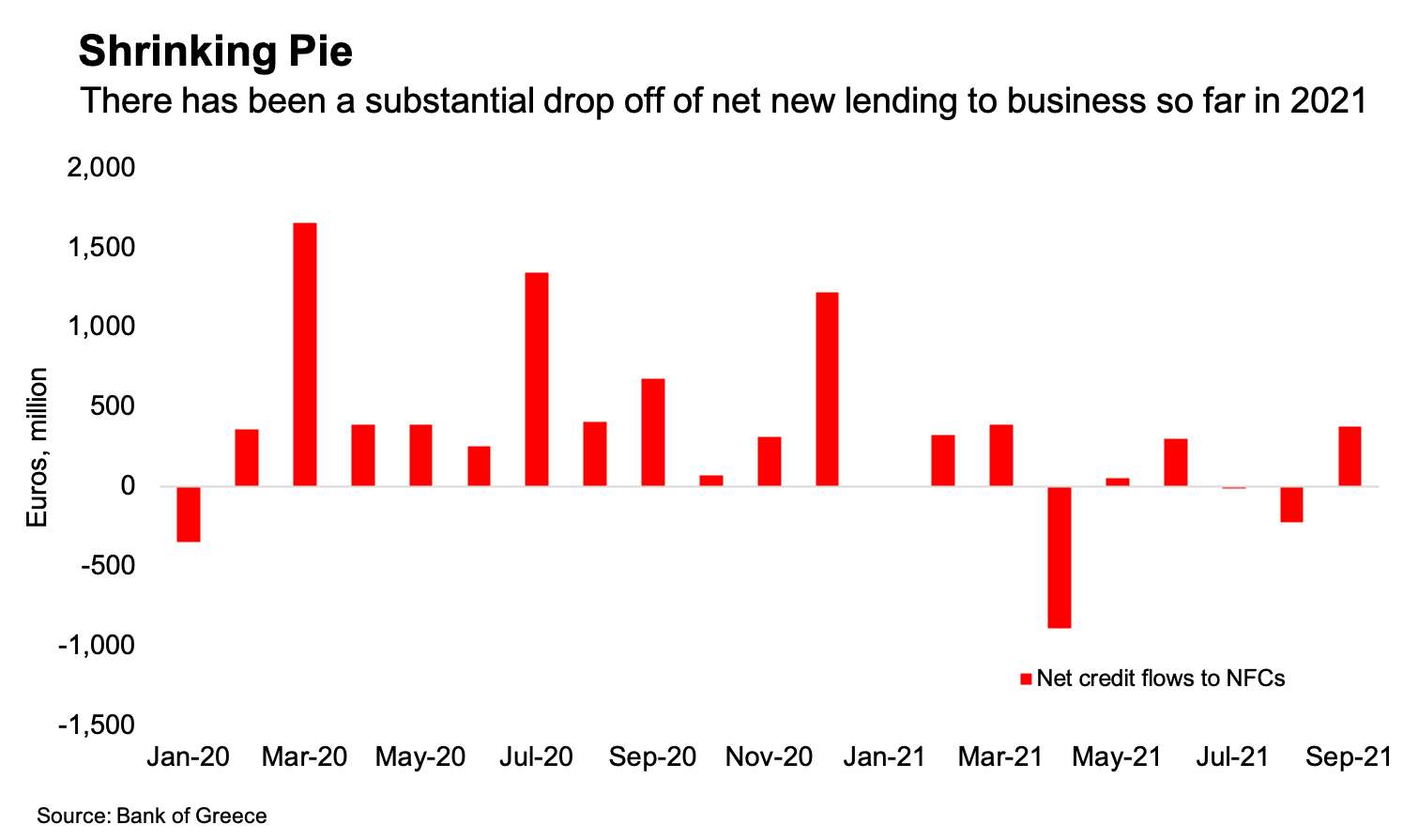

The latest figures from the Bank of Greece show that the flow of net lending to businesses actually turned positive again in September, even if the annual growth continued the decline. Still, in the first nine months of the year there was just 283 million euros of net new lending to non-financial corporations, compared with 6.7 billion euros for the whole of 2020.1

Stripping out debt securities to look at just loans, credit flows to businesses were actually negative between January and September, with a negative net lending flow of 240 million euros.

The banks have taken some mild political heat for not lending more, so some of the briefing by bank officials is to publicly say that they’re trying their best.

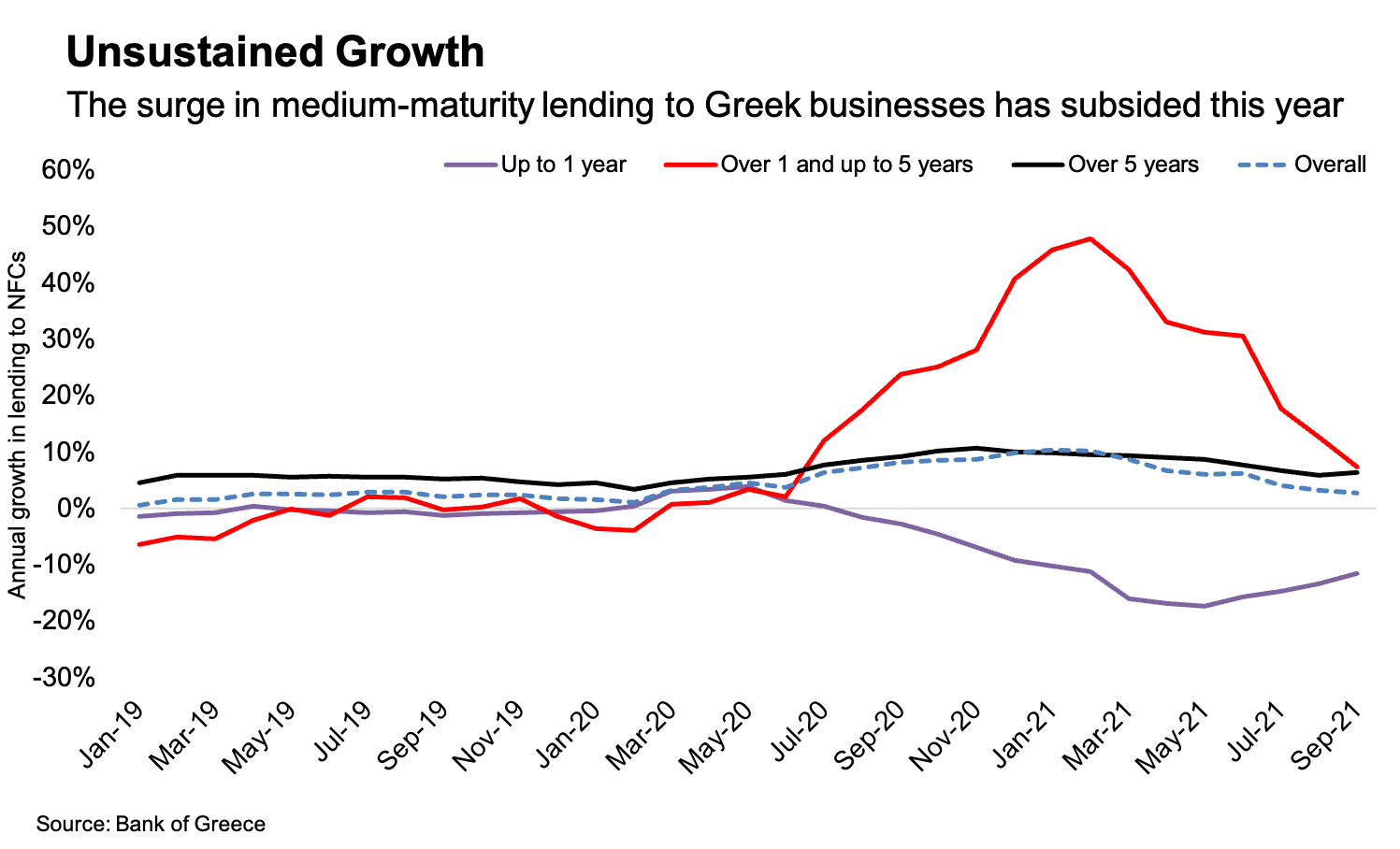

And it would appear true that the crisis has given companies — including small and medium-sized enterprises — the opportunity to change the term structure of their liabilities. In the first news story linked above, bank officials are complaining that companies used subsidised working capital loans under the TEPIX programme to pay off existing bank loans.

That’s backed up by Bank of Greece data that show spikes in flows to credit to SMEs last year in months corresponding to TEPIX deadlines. The data also show a surge in lending for maturities of between two and five year — TEPIX working capital loans have two-year maturities — with drops in short-term lending.

Total bank lending to SMEs amounted to 6 billion euros in 2020 and 2.5 billion euros in the first nine months of this year. However, after subtracting the amount flowing back to the banks, those figures drop to 2.2 billion euros of net new lending in 2020, and just 267 million euros so far this year.

If it were the case that SMEs have all the access to finance that they need and are just sitting on their eggs (to use a Greek expression), this would only be a problem for banks seeking to increase profit margins. However, that isn’t the case.

Last week the Bank of Greece released the lending survey for the third quarter, which showed that demand picking up for all categories of loans since the second half of last year. It also shows there was a slight increase in the ratio of rejected applications in the last quarter.

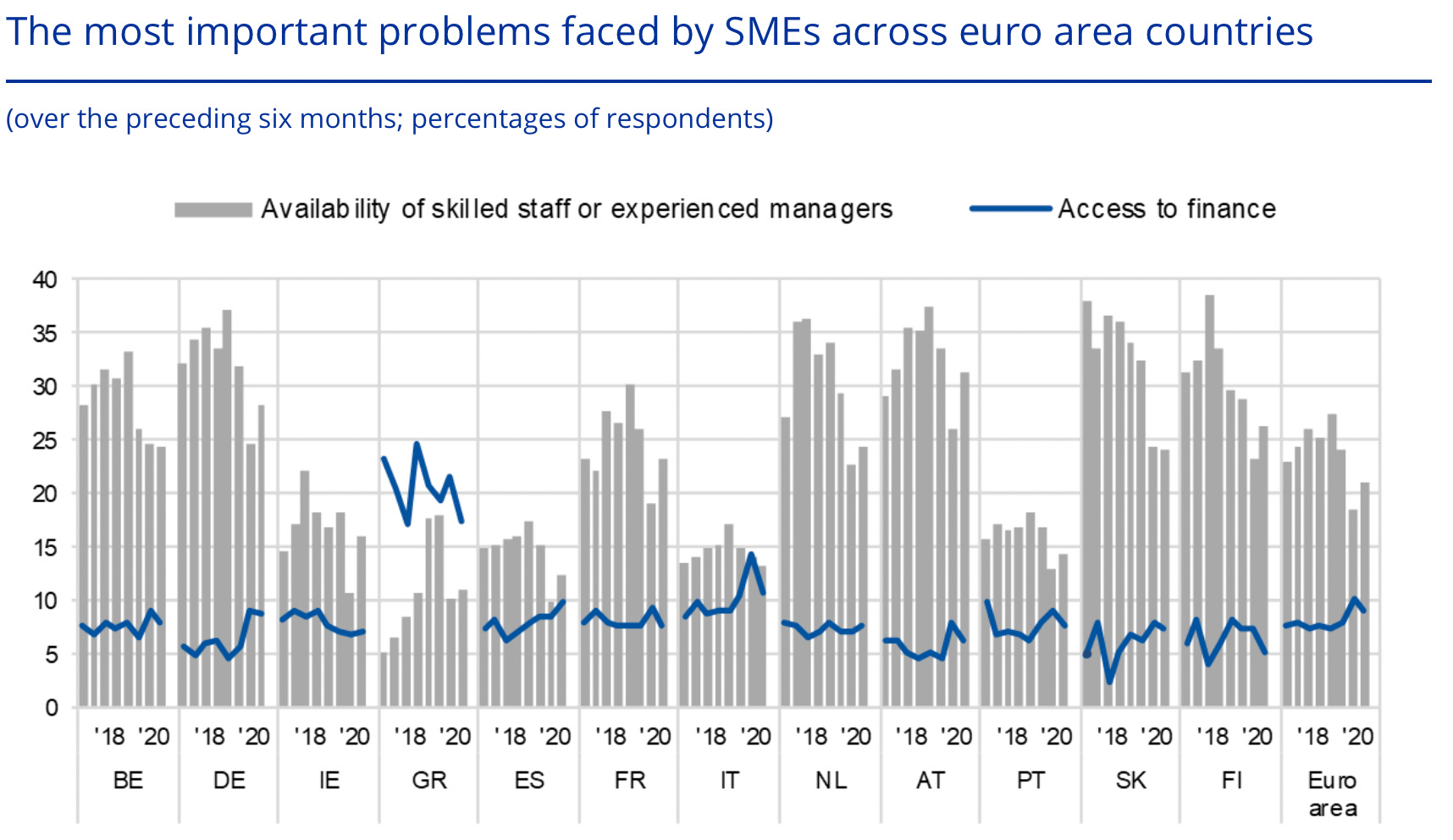

The European Central Bank’s most recent survey on the access to finances of enterprises, published in June, shows that Greece is a clear outlier in the euro area in the extent to which access remains a major problem for SMEs. According to the survey, 18 percent of SMEs cited it as the biggest problem they faced, with 22 percent of firms reporting difficulties in accessing bank loans.

The survey also underlined the importance of government support in the absence of further access to bank financing, showing that 56 percent of SMEs had received some form of support other than wage support and tax cuts.

Of the 21 percent of Greek survey respondents that said that bank loans were not a relevant source of finance for them — the highest in the euro area — a striking proportion gave high interest rates as the reason, as can be seen in the last of the three charts above.

We looked at this subject a two months ago — credit growth in Greece is constrained by interest rates that are considerably higher than elsewhere in the euro area. The central bank released loan and deposit rates for September today that suggest there hasn’t been much improvement since. The average interest rate for new loans to SMEs only dropped to 3.24 percent from 3.3 percent in August.

Yes, credit risk is an issue. But it’s worth remembering that as of September the banks had borrowed 46.9 billion euros from the European Central Bank at negative interest rates from the TLTRO programme — which is tied to targets for extending credit to the real economy.

This is the problem with claims from the banks that the obstacle to increasing lending is that companies have access to cheaper financing from the government. It’s not backed up by data. It does show that state liquidity support has been crucial for the survival of businesses — but bank loans could also still have a bigger role to play if they were cheaper and more accessible.

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.

September’s jump also looks suspiciously like it may be the result of a small number (possibly even just one) of very large projects. The Bank of Greece today released data on deposit and loan interest rates, which show that there were 1.38 billion euros of new loans with a defined maturity over an amount of 1 million euros — over 90 percent of all new loans. There’s a 51 basis-point drop in interest rates in this category to 2.52 percent. This sticks out as the other categories aren’t much changed, which does look like a whale moved the series.