Macro roundup: The weakest link

Greece's debt crisis legacy lives on in bank interest rates and credit bottlenecks

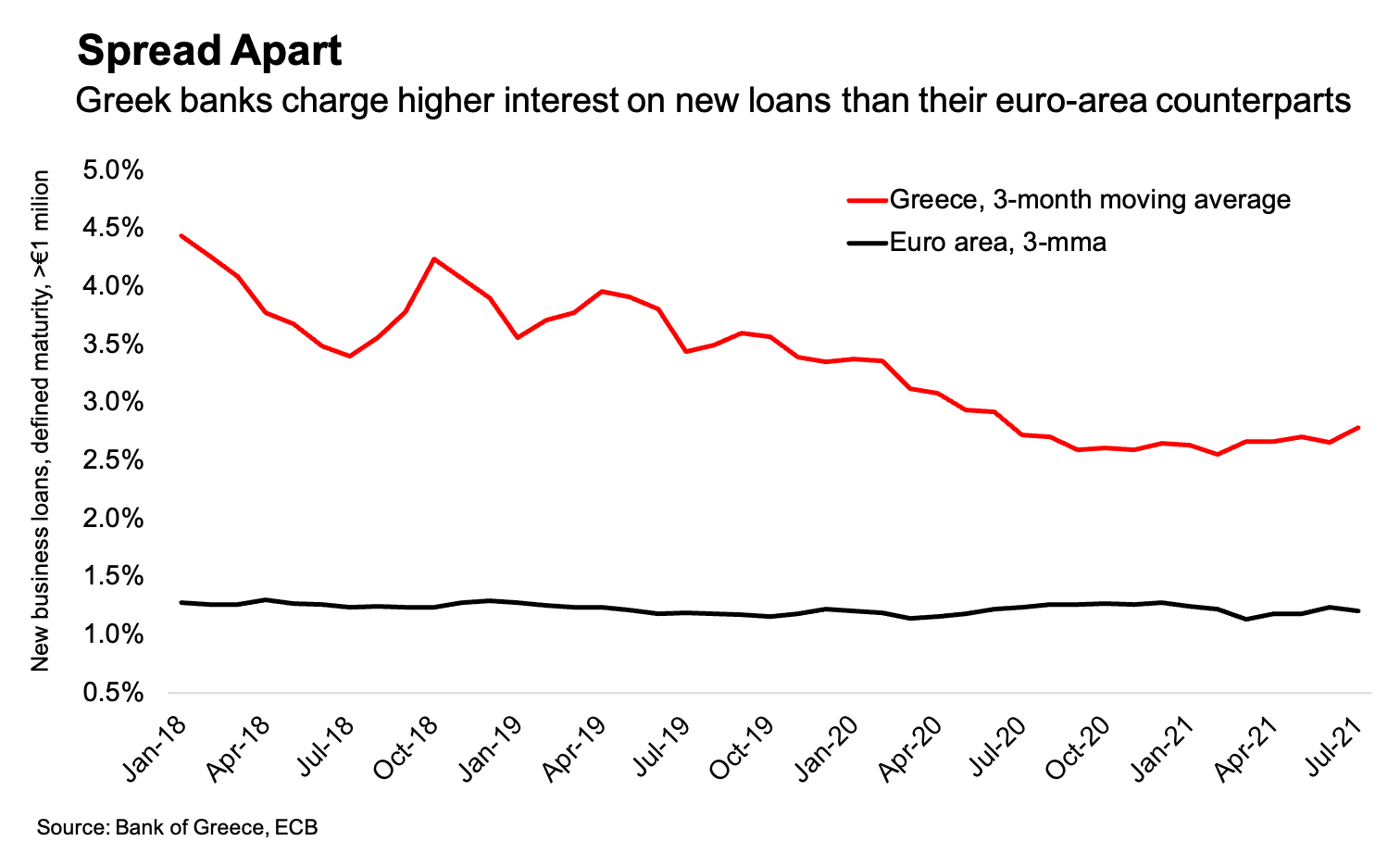

After last week’s look at how credit growth has stalled this year, a reader drew my attention to the high rates of interest Greek banks continue to charge businesses and households compared with the rest of the euro area.

The Bank of Greece this week released data on loan and deposits interest rates that underlined this point. The average rate for a business loan with a defined maturity was 3.21 percent in July, compared with a euro-area average of 1.36 percent. Greece’s rate has risen 60 basis points since September 2020, when it was 2.61 percent.

The average rate for a housing loan in Greece was 2.58 percent, compared with a euro-area average of 1.31 percent. Overall, the country’s weighted average interest rate for all new lending to households and non-financial corporations stood at 3.99 percent in July.

The most alarming aspect of the trend is the lack of convergence towards the euro-area average — particularly in recent months. The proportion of bad loans sitting on the banks’ balance sheets peaked at almost half the total in 2017 — a legacy of the country’s debt crisis that kept new credit at such depressed levels.

But the government’s Hercules asset protection scheme allowed the banks to take more than 20 billion euros of bad loans off their balance sheet last year through securitizations. With a similar amount to follow under the successor Hercules II program, all four of the country’s systemic banks say that they will bring their ratio of bad loans — or non-performing exposures, to use the jargon — down to single digits within 2022.

The reader who wrote after last week’s post pointed out that the main reason for rates to be so high was to have enough earnings to afford the impairments on the bad loans. Following the securitizations, rates should be significantly lower. But in their business plans, banks are giving guidance that rates will remain quite flat up to 2024.

Just capital

This brings us back to Bank of Greece governor Yannis Stournaras’s regular criticism of the banks’ failure to provide more credit to the real economy. This usually comes with the central bank chief noting that the Hercules scheme, while getting bad loans off the banks’ books, does little to resolve their other problem of a weak capital base.

Stournaras spent the years from 2018, when the Hecules plan was forming, touting the central bank’s own bad bank plan — which he argued would tackle the capital problem by also transferring the banks’ deferred tax credits onto the asset management company that would be created. His plan won fans in the International Monetary Fund, but not the banks themselves.

So in 2021 we’ve seen the banks still focussed on boosting their capital, with Piraeus Bank and Alpha Bank both proceeding with share capital increases. The latter tapped investors using the novel marketing pitch that it was a “growth capital increase”, aimed at positioning the bank to go big on lending to the real economy under the guise of Greece’s national recovery plan.

Meanwhile, credit growth is stalling while Greek borrowers face costs that are substantially higher than the euro-area average for bank loans.

That adds to the attraction of other sources of liquidity for businesses large enough to ride the wave of capital market appetite for corporate debt. In the first half of this year, non-financial corporations issued 1.48 billion euros in bonds in Greece. That’s more than any full-year total since 2008, when 5.84 billion euros of corporate securities were issued.

Other data

The manufacturing purchasing managers index rose to 59.3 in August, signalling the biggest improvement in operating condition since 2000 as economies reopen. However, IHS Markit again flagged rising input prices and supplier shortages.

Greece’s economic sentiment indicator also improved in August, according to the European Commission — although consumer confidence continued its recent slide.

Retail sales rose 11.7 percent in June from a year earlier as base effects from the pandemic — and fluctuating energy prices — continue to work through.

If you’re enjoying this newsletter, consider sharing it with others who might also like it.

Next week’s key data

Tuesday, Sept. 7:

Second-quarter gross domestic product (Elstat)

July commercial transactions (Elstat)

Friday, Sept. 10:

August consumer price index (Elstat)

July industrial production (Elstat)

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.