Choppy waters for bonds

In a rising-yield environment, it makes sense for Greece to issue new securities early

Despite a shaky start to the year for European sovereign bond markets, reports suggest that Greece’s public debt management agency intends to get as much as it can of its planned issuance for 2022 out of the way as early as possible.

This makes sense; if market conditions are less favourable now than they were in the first half of 2021, they’re unlikely to get much better as 2022 progresses. The yield on Greece’s benchmark 10-year bonds is currently 1.54 percent, up from a record low of 0.53 percent in August.

A mini-rally after last month’s announcement that the ECB had flexibility to increase Greek government bond holdings after March, when its Pandemic Emergency Purchase Programme ends, proved short lived. Already this year the 10-year yield rose around a quarter of a percentage point.

Of course, this is not predominantly a Greek story now but a global macro story about inflation persisting and the U.S. Federal Reserve’s hawkish turn. This raised expectations that central banks will hike interest rates more aggressively than previously expected. Even Germany’s 10-year bond yield is on the brink of turning positive, even though the is ECB currently the most dovish major central bank.

Still, Greece is facing pressures of its own, which are likely to come to the fore as the year progresses. As we noted in the last newsletter of 2021, the central bank’s shift in stance — from one where it is steadily hoovering up more than 1 billion euros a month of Greek government bonds to a looser commitment after March to step in to stabilise conditions if needed — creates a situation where markets will likely test what price level it would take to trigger this “Lagarde put”.

But even without the looming end to PEPP, the central bank can’t continue the current rate of purchases indefinitely. That would soon lead to it running out of securities to buy.

So for the PDMA to front-load its bond issuance has the dual benefit of getting the bulk of the year’s goal completed before market conditions worsen, while also increasing the eligible universe of bonds that the central bank could buy.

The agency plans to issue 12 billion euros of bonds this year, with 8 billion euros of amortisation due on existing debt. The PDMA also plans a reduction of the T-bill stock and early repayment of bailout debt amounting to a combined 5.2 billion euros.

The government’s overall financing needs for this year amount to 24.8 billion euros, and part of that will be met by a 6.6 billion-euro reduction in its cash buffer, according to the PDMA’s 2022 funding strategy. The cash buffer at the end of last year stood at 31.6 billion euros.

The maintenance of a cash buffer in excess of 30 billion euros — which reduces the country’s refinancing risk — has been a centre-piece of Greece’s macroeconomic management since the county exited its bailout in 2018.

Thanks to the cash buffer, the government was actually a net domestic creditor rather than a debtor between the bailout exit and the start of the pandemic. The shifting monetary landscape subsequently upended that picture.

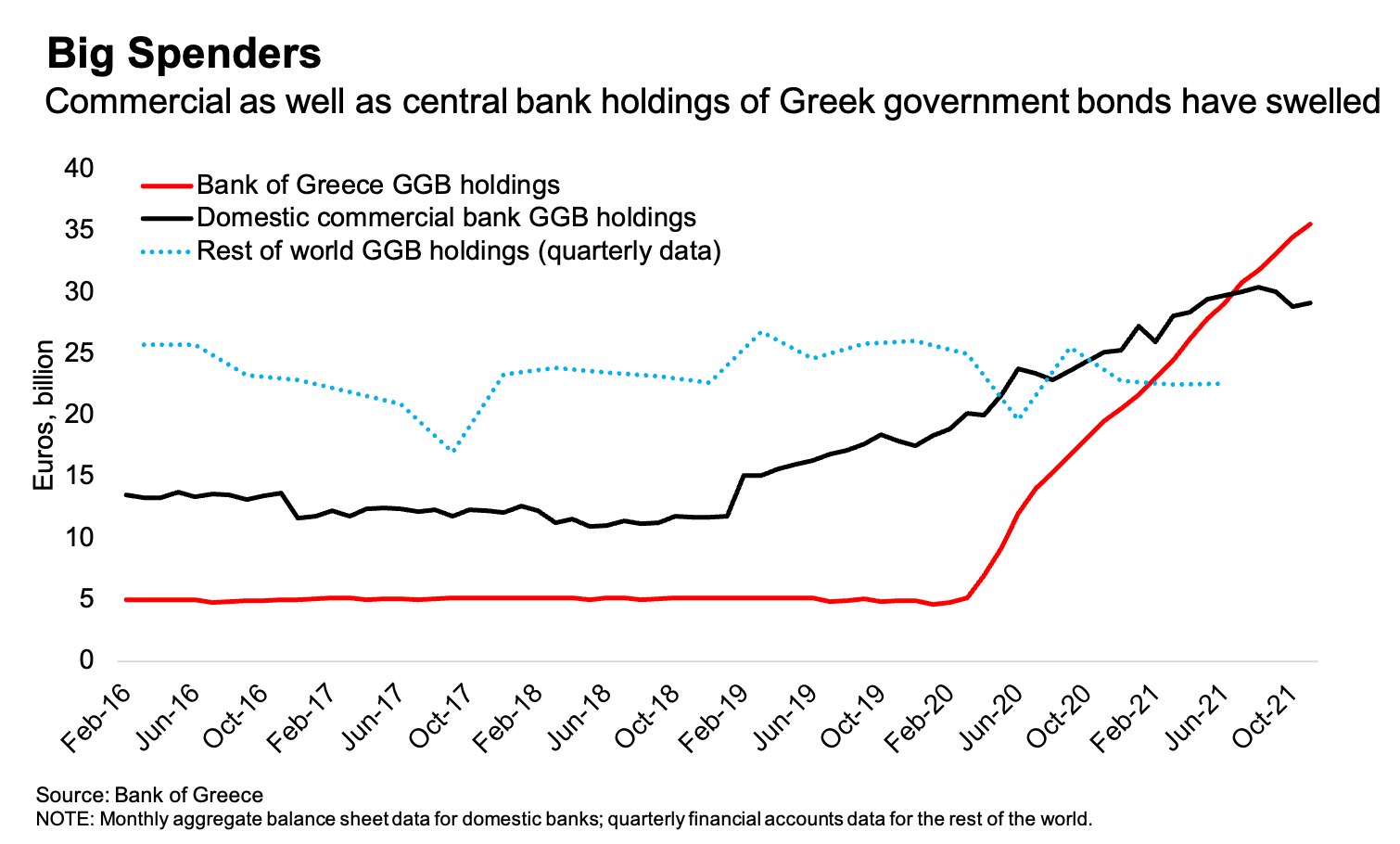

Not all domestic holdings of Greek government bonds are quite what they seem, however. The major driver of the increase in the net domestic debt is the the Bank of Greece’s PEPP purchases. In essence, this is really a liability to the rest of the euro area. But since operationally the ECB’s asset purchases are carried out by national central banks, it appears as a liability to the domestic financial system.

This is seen in the sudden surge in the central bank’s bond holdings in the chart below. However, it’s not only about Bank of Greece puchases. Domestic commercial bank holdings also increased by 12.3 billion euros.

While a part of that can be attributed to an appreciation in the market value of their holdings, the flow of long-term government securities to the banks also amounted to 7.7 billion euros in 2020 and the first half of last year. During the same period, rest of the world flows amounted to a reduction of 8.6 billion euros.

With PEPP winding down, this presents a tricky situation.

The commercial banks have been under fire since the first year of the pandemic from the Bank of Greece’s governor, Yannis Stournaras, for using the surge in ECB liquidity to increase their holdings of government bonds and central bank reserves, instead of extending more loans to households and businesses. But if they stop buying government bonds now, who’s left as a major buyer in this market?

The banks’ exposure to government bonds in a rising yield environment could also impact their profitability as they complete their massive programme of bad-loan securitisation. Trading gains on government securities in 2020 helped cushion the blow from the losses they had to swallow to get the non-performing exposures off their balance sheets.

Profits from their government bond holdings are unlikely to give them the same assistance this year, as they try to finish the job of getting the ratio of NPEs to total loans into single-figures this year. That will add to the pressure on capital ratios — their Achilles heel — and it will continue to raise questions about how able they are to provide the long-promised increase in lending to the real economy.

Careful handling of this situation is needed to avoid a recurrence of the “sovereign-bank doom loop” that was a characteristic of the eurozone crisis. Presumably the ECB will have intervened by this point, with the “under stress” condition triggered.

The credit rating agencies are the deus ex machina in this, as it would considerably ease the situation if one of them raised Greece’s sovereign debt rating to investment grade (S&P and Fitch both have it two tantalising notches below).

Aside from then making the bonds eligible for the ECB’s regular Asset Purchase Programme — rendering moot the question of when the central bank might increase its PEPP holdings of Greek bonds — it would also open the country to flows from portfolio managers required to hold only investment grade securities. That might then provide part of the answer to the earlier question of who would be a buyer of Greek bonds right now.

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.