More on Greece's terms of trade improvement

Looking at refining, services and the price of exports over imports

Macroeconomic statistics can sometimes throw up anomalies, and when that happens, it’s good to maintain a healthy degree of scepticism. We talked about one such anomaly in last week’s macro roundup, when we noted that Greece’s terms of trade significantly improved in 2022 according to the official data.

Given that the terms of trade of almost every other euro-area country deteriorated last year — often quite sharply — my gut feeling is that this is a statistical artefact that will be smoothed out in subsequent revisions of Greece’s gross domestic product numbers.1

That said, it’s good to keep an open mind. We didn’t look much last week at the reasons why Greece’s terms of trade might have improved, so this follow-up post aims to scratch a little deeper.

Refined goods

A first thing to consider is that although Greece is a net energy importer, oil products have nevertheless become an increasingly important part of the country’s export mix in the last two decades thanks to the growth of its refining sector.

As a result, oil accounted for 17.8 percent of all goods and services exports last year, compared with just 2.1 percent in 2004. Of course, oil imports have risen in parallel, since Greece’s refining sector requires oil inputs. But as long as the price for refined petroleum products grew faster than for unprocessed inputs, that worked to the benefit of the country’s terms of trade.

Unfortunately, the GDP numbers, which we’re using to get a measure for the terms doesn’t break down the data for oil or energy imports and exports. That means using data from the balance of payments to back of envelope calculations on the impact, but mixing data sources is not ideal, so the analysis comes with a health warning.

The balance of payments data is published in nominal terms only, but the Bank of Greece does note in its press releases how much exports and imports changed at constant prices. We can take those number to calculate the implied inflation in goods imports and exports in the central bank’s statistics.2

Part of the reason why I didn’t examine the impact of oil exports on the terms of trade last week was because its hard to envision a sector that still accounts for less than of a fifth of total exports turning Greece into such a big outlier. I remain sceptical, but have to concede the numbers are quite striking.

Lower volumes, higher margins

Using the balance of payments data, the price of Greek exports in goods increased 30.4 percent last year, while goods import prices grew 19.8 percent.3 That's largely driven by the price of oil exports, which increased 78.5 percent. Price inflation for non-oil goods exports was 15.2 percent.

The price increase for oil imports, while still extremely high, at 57.7 percent was markedly less than for exports. Non-oil goods import prices rose 7 percent.

In fact, the Bank of Greece’s figure shows that while the volume of oil imports grew 21.2 percent last year, the volume of oil exports actually dropped by 3.4 percent.

Greece has two big refining companies, Hellenic Petroleum and Motor Oil Hellas. Unfortunately, the latter hasn’t published its full-year results for 2022 — but what we have from Hellenic Petroleum and from Motor Oil’s nine-month earnings does support the picture of lower export volumes and higher margins. For Hellenic Petroleum, it looks like exports of net production dropped 21.4 percent last year.

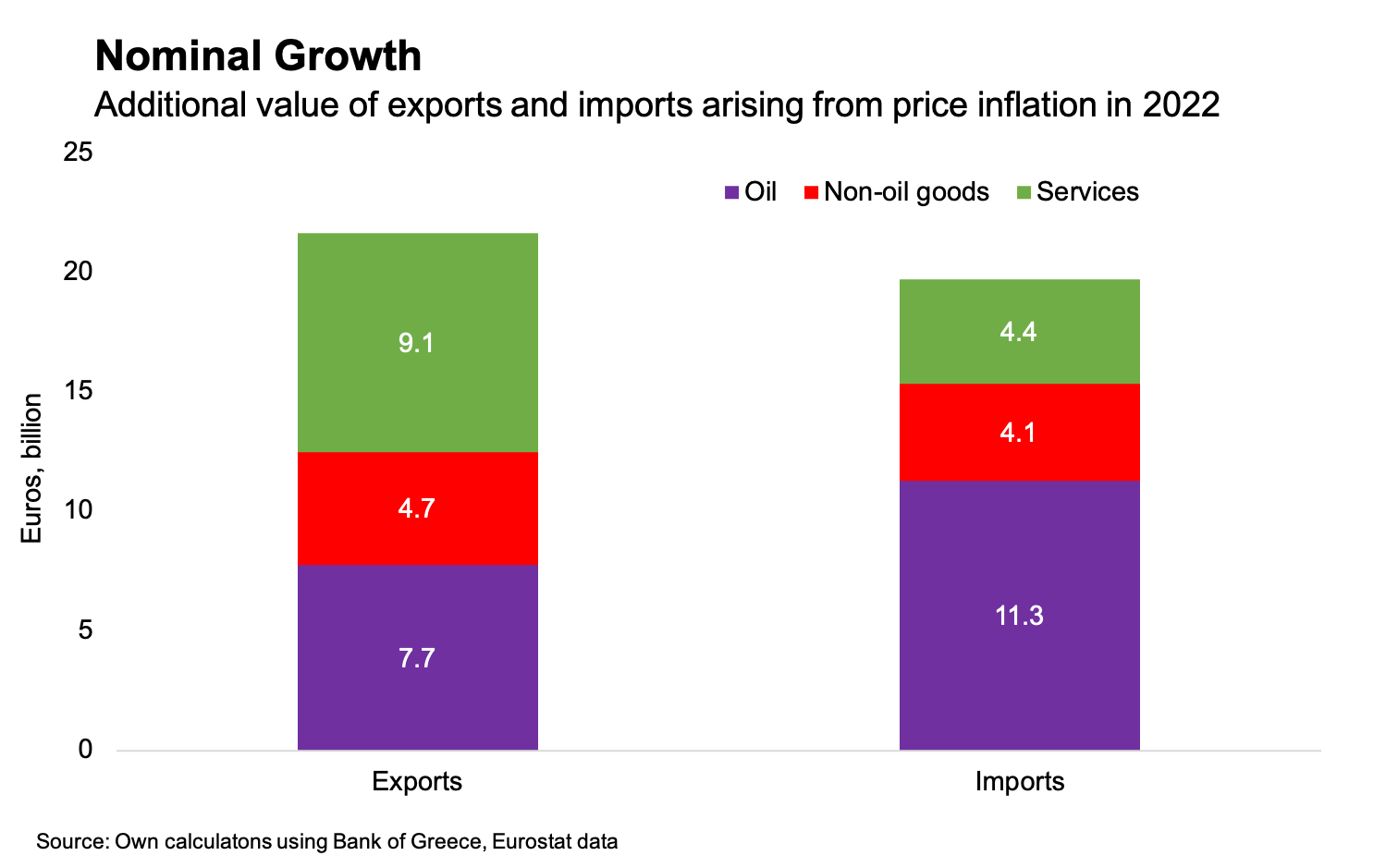

The chart above attempts to estimate the additional value of exports and imports that are due entirely to price inflation. It takes the nominal value of exports and imports in the balance of payments data, then subtracts the values at constant 2021 prices.4 It finds that inflation added 21.6 billion euros ot the value of total exports last year, or 21.4 percent of the total. Imports added 19.7 billion euros — 16.3 percent of the total.

Murky services

Despite the higher price growth in both oil and non-oil goods exports compared with imports, inflation added more to the absolute value of than goods imports than exports. As usual, it was services that made the difference. Unfortunately, we have even less granular data for services to deconstruct than we do for goods.

We do see in the GDP data that the price of service exports increased 23.8 percent while the price of service imports increased 18.5 percent. As with goods, these increases are among the highest in the EU.

To conclude, Greece’s balance of payments statistics provide a plausible explanation for how the increase higher prices for refined petroleum products could have caused such a marked improvement in the country’s terms of trade.

However, I find it striking that Greece’s rate of price increases for both exports and imports, in both goods and services, are all at or near the top of the EU charts. That is partly why, in my view, the Occam’s razor explanation for the jump is that it is part of the iterative process whereby the accuracy of economic statistics improves as more data is incorporated with subsequent releases.

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.

The only other eurozone countries that saw a terms of trade improvement were Estonia and Ireland, but in both these cases it was to a much less significant degree than Greece. And Ireland’s GDP data is notoriously weird.

I’m going to try very hard to avoid using the term “deflators” in the post, as it’s confusing.

That health warning comes in here, the GDP data show inflation being higher for both of these, with the price of goods exports increasing 36.5 percent import prices rising 26.3 percent. On the export side, both the GDP and the balance of payments data make Greece’s price increase comfortably the highest in the European Union.

Here comes the health warning again. The Bank of Greece press releases don’t give any information on the change for services at constant prices, like it does for goods. So I’m calculating these using the deflators in the national accounts data, while using the balance of payments deflators for goods exports and imports.