Macro roundup: Unemployment trends down

Greece's jobless rate drops to 10.9%; demand for bank credit falls; manufacturing improves

Greece’s unemployment rate is getting close to returning to single digits for the first time since 2009 after another decrease in March.

The seasonally-adjusted jobless rate dropped to 10.9 percent from a revised 11.3 percent in February, according to the Hellenic Statistical Authority. Although the rate was even closer to single digits in January, at 10.2 percent, unemployment remains on the steady downward trend that it has been on for the past decade. The youth unemployment rate in March was 24.2 percent.

As it’s a lagging indicator, the unemployment rate is one that we often don’t look at closely. But it’s worth periodically remembering that in July 2013, at the height of Greece’s depression, the rate peaked at an astonishing 28.1 percent — with the youth unemployment rate around double that. It’s been a long road back from that point.

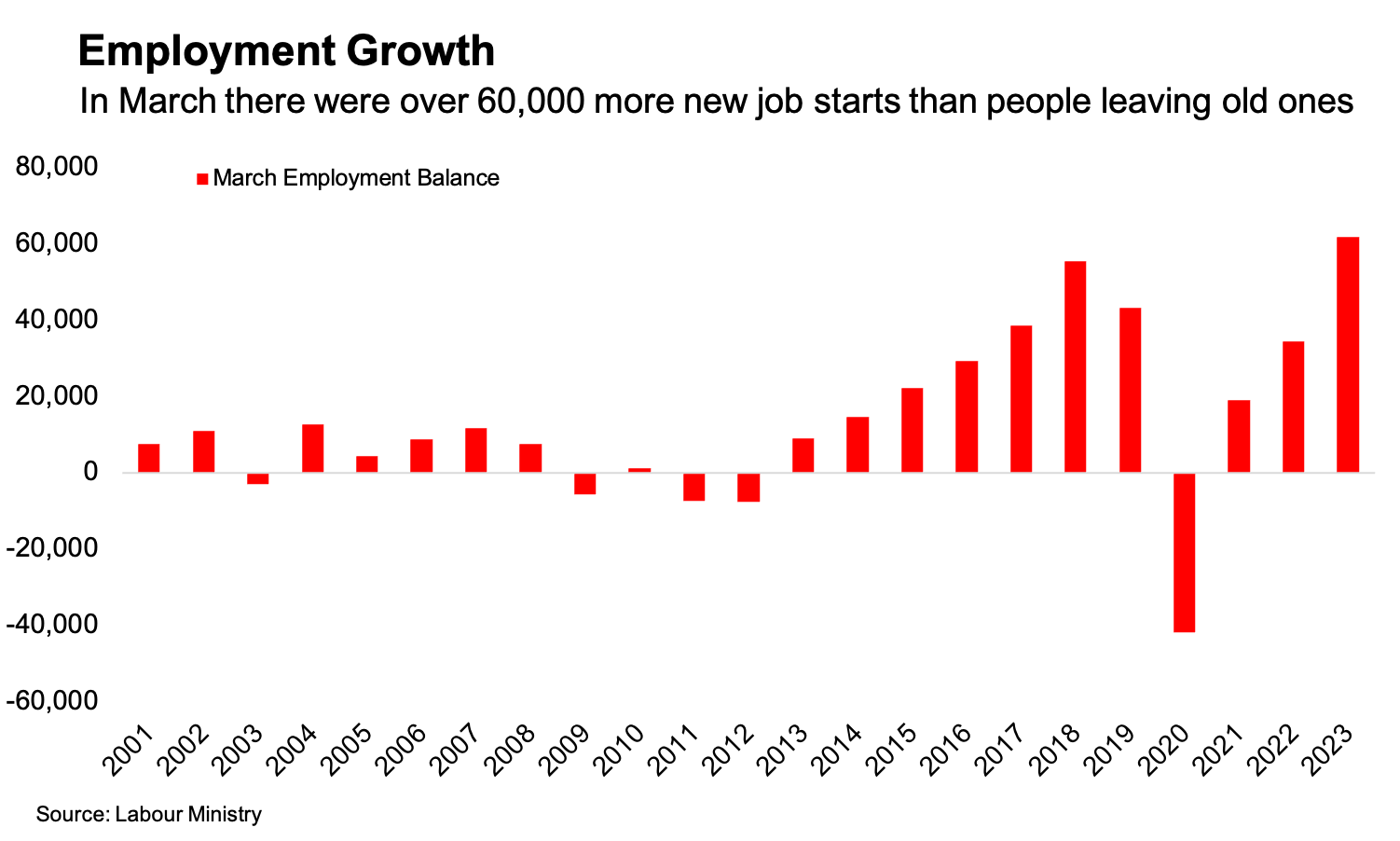

Figures from the Labour Ministry, which publishes employment balance data comparing the numbers of people leaving jobs and with those starting new ones, confirm that March was a strong one. These showed a positive employment balance of 61,912, which is the most for the month of March since Greece joined the euro.

Digging deeper into the Labour Ministry figures, the sector with the largest employment balance was accommodation, with 24,150, followed by restaurants and catering with 5,630. Although it is still early in the year, this does hint at early expectations of another bumper tourist season in 2023.

Credit conditions

The Bank of Greece this week released data on lending and deposits in March, which showed some reversal of the tightening conditions that were apparent in the previous month’s release.

The annual growth rate in lending to the private sector ticked up to 5.1 percent from 4.8 percent in February. Lending flows were positive in the month, with 1.17 billion euros in net new lending following an increase of just 27 million euros in February and a drop of 2.02 billion euros in January.

On other side of the ledger, there was a 2.32 billion-euro increase in private sector deposits, following a cumulative drop of 5.97 billion euros in the first two months of the year.

But signs of conditions tightening are apparent in the Bank Lending Survey for the first quarter, in which loan officers reported a drop in demand for new borrowing for business loans as well as mortgages.

Speaking at the Delphi Economic Forum last week, Eurobank’s chief executive officer, Fokion Karavias, attributed the drop in demand to higher interest rates for new loans.

Fat margins

March was a month of banking turmoil outside Greece, but this didn’t amount to much increase in interest rates for depositors. The average weighted interest on new deposits crept up to 0.23 percent from 0.21 percent the month before.

For new loans, the weighted average interest rate increased to 5.73 percent from 5.57 percent. This mean that interest rate spread, which was already at record levels, rose another 14 basis points in March to 5.5 percent.

Other data

Greece’s manufacturing Purchasing Managers’ Index dipped slightly to 52.4 in April from 52.8 in March

A reading above 50 signals improving operating conditions, so April’s data was still consistent with an expansion in the sector

Job creation was the fastest in a year, while new orders growth accelerated, according to S&P Global, which produces the report

Policy platforms

Greece’s election is now less than three weeks away, so we’re right in the thick of the campaign. However, the May 21 vote will almost certainly fail to produce a new government, so we’ll probably head back to the polls on July 2.

Although a lot can happen between now and then, the likeliest outcome from the second vote is that Kyriakos Mitsotakis returns to power at the head of a New Democracy-Pasok coalition government.

So, what has Mitsotakis committed to on the macroeconomic front for his second term? The prime minister unveiled his manifest last week. Here’s how Kathimerini reported these:

Mitsotakis reiterated “our non-negotiable goal is to increase wages by 25% within four years, so that the average wage reaches 1,500 euros,” while promising twice the EU growth rate, doubled public investment and a 70% increase in total investment, along with cutting the public debt to 140% of GDP in 2027 and 120% in 2030, and the restoration and maintenance of inflation at 2%.

He also promised investment in healthcare and education, continuing with the digitisation of the public sector so that 90 percent of the state’s services are on the gov.gr platform, and speeding up judicial processes.

For Syriza, the main opposition party, central planks of the economic platform include lowering VAT and reintroducing primary residence protection from foreclosure, as well as pledging to increase public sector wages.

However, the party is currently polling about 5 to 6 percentage points behind ND. If they finishes in second, getting a mandate to form a government would require not just collaboration with Pasok, but also the support, explicit or tacit, of Yanis Varoufakis’s party, MeRA25, and/or the Communist Party of Greece. It would probably require both those parties.

Getting all those parties under the same umbrella is, frankly, not going to happen. Given the size of the lead they’d need to overturn in order to come first, a return to power of Syzria and its leader, Alexis Tsipras, looks unlikely.

Next week’s key releases

Monday, May 8:

March commercial transactions (Elstat)

Wednesday, May 10:

April consumer price index (Elstat)

March industrial production (Elstat)