Macro roundup: GDP surprise

The 8.2 percent contraction in 2020 was smaller than many expected

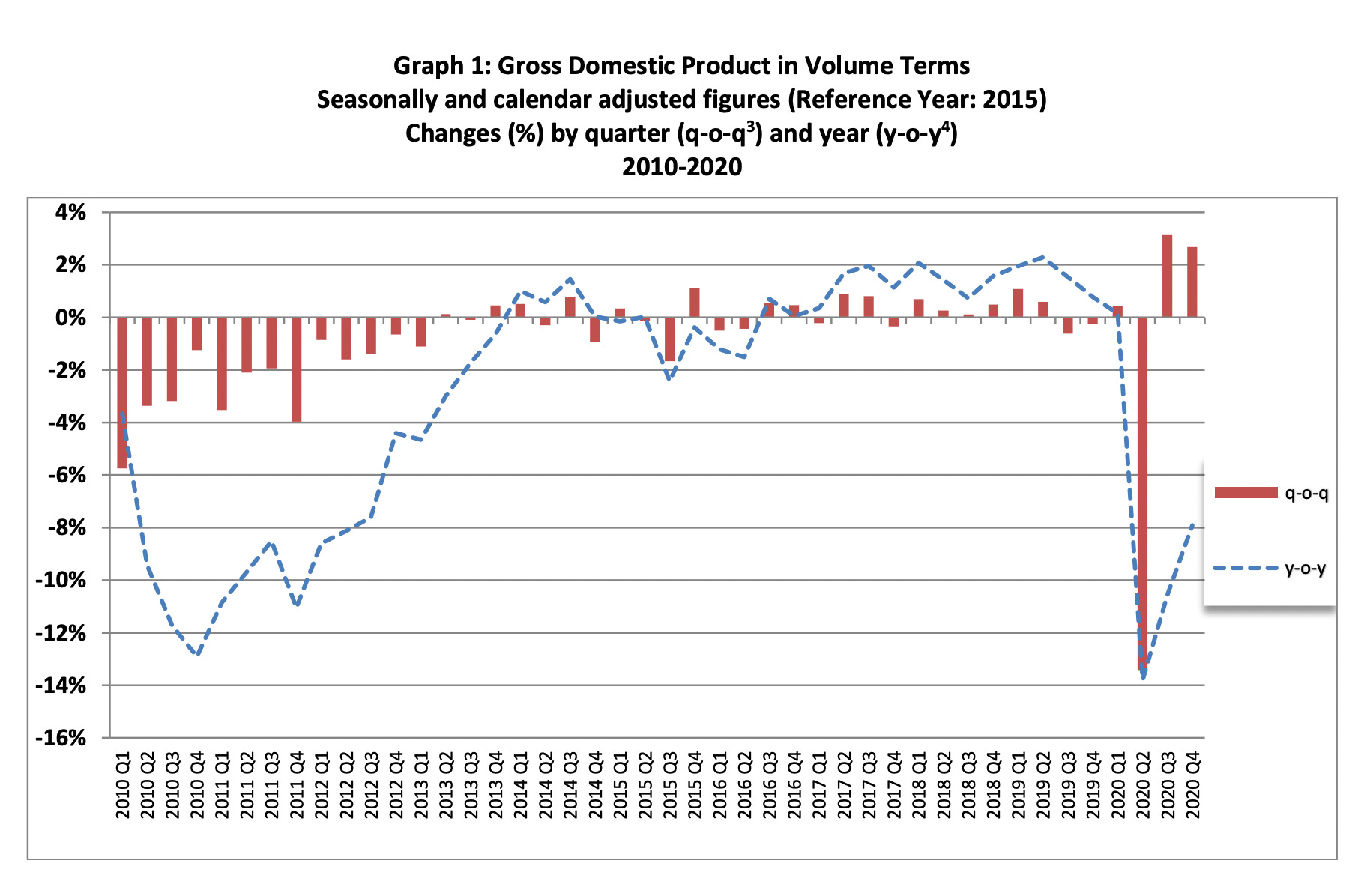

It was all set to be a quiet week on the macroeconomic front until Elstat yesterday brought forward Monday’s scheduled release of the fourth-quarter GDP numbers to today instead. And everyone has been quite pleasantly surprised by the outcome (if not by the amount of notice we received).

With the Finance Ministry forecasting in the budget that the economy contracted 10.5 percent last year, and the European Commission estimating a 10 percent drop in economic activity, the big surprise in today’s figures was that the contraction for the whole year was restricted to 8.2 percent.

Gross domestic product in the fourth quarter shrank 7.9 percent compared with the same period of 2019, but on a quarterly basis, output increased 2.7 percent from the third quarter (when it grew 3.1 percent).

I’ll just drop in the chart from the release here:

Caution is needed when interpreting the results as Greece’s GDP data is subject to unusually large revisions even in normal times — and these are obviously not normal times. For example, in the last three releases, including today’s, the quarter-on-quarter reading for the last three months of 2019 has swung from -0.9% to +0.5% to -0.3%.

It’s also worth noting that deflation last year averaging 1.2 percent also had a bearing on the real GDP. In nominal terms, GPD last year dropped 9.6 percent.

Here’s what I wrote after the third-quarter GDP release:

The government’s outlook for this year could be a little too bleak — especially since this quarter’s release contained revisions to last year’s data that add 0.5 percent of GDP growth to this year’s figures due to a statistical technicality known as the “carry-over effect”.

Adjusting for this impact, a 10 percent GDP contraction this year would imply GDP shrinking 14.5 percent in the fourth quarter compared with the same quarter in 2019 (the big caveat here is that more revisions to the data, which are common, would affect these calculations). If that happens, it would mean the current lockdown having an even bigger impact on GDP than the one in spring.

Setting aside the technicality about the carry-over effect (small impact), the point about the size of the fourth-quarter contraction held up in the end.

The second lockdown would have needed to be much more damaging than the first to push Greece into such a big annual contraction (given today’s figures, it would have taken a 15.8 percent year-on-year contraction in the fourth quarter, compared with the 13.8 percent drop in GDP we saw in the second quarter).

Given the revisions, and, relatedly, the challenge this extraordinary year presents for seasonal adjustment, I’ve been wary of looking too much at what the GDP components have been doing quarter-by-quarter.

But now that we have the first full-year figures for 2020, it is worth a quick rundown on the annual components:

Final consumption: -3.4%

Houeholds and non-profit institutions serving households: -5.2%

Government consumption: +2.7%

Gross capital formation: +4.9% (the increase was mostly due to inventories, though it looks like fixed investment basically held up)

Exports: -21.7%

Imports (a negative number contributes positively to GDP): -6.8%

Other data

Greece’s manufacturing PMI dipped to 49.4 points in February from 50 points in January, according to the latest data from IHS Markit. That signals a shift from unchanged operating conditions in manufacturing to things getting worse. Markit also flagged up escalating cost inflation.

Greek banks’ reliance on ECB liquidity rose 2.28 billion euros after not much change in October and November. A similar pattern was observed in the third quarter, so it’s either a coincidence, or the banks have some reporting reason for these end-quarter jumps. But if there is a reason, I don’t know what it is yet.

From the same source — the Bank of Greece’s balance sheet — the central bank’s TARGET2 deficit against the rest of the Eurosystem jumped 5.15 billion euros to 80.3 billion euros in December, the biggest increase since June. Due to a quirk of the financial calendar we get data a bit later for December than we do for other months, so it wasn’t available last week when we looked at the balance of payments. Now we have this, we can chart the full-year financial account, disaggregating the T2 balance from “other investment”, as we’ve been doing.

If you’re enjoying this newsletter, consider sharing it with others who might also like it.

Next week’s key data

Wednesday:

February consumer price index (Elstat)

January industrial production (Elstat)

Thursday:

December building activity (Elstat)

Elsewhere on the web

Once more, I’m going to hold off on “elsewhere on the web” today. So you’ll get two weeks’ worth next Friday.

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.