Macro roundup: Squeaky bum time

The government needs to hold its nerve on fiscal support as bills start to mount

This has been a quiet week in terms of macroeconomic releases, with trade data from the Hellenic Statistical Authority showing that December’s deficit was slightly better than 2019, and manufacturing sentiment indicating stabilising conditions in January.

But perhaps the most important — and alarming — development has been the slight note of panic emanating from the Finance Ministry about the escalating toll of the pandemic on the state budget. Earlier this week Finance Minister Christos Staikouras admitted on radio that the cost of supporting the economy this year will be higher than the 7.5 billion euros in the 2021 budget, and subsequent press reports have stressed how the government is trying to scrimp extra funds for Covid relief.

This newsletter has long beaten the drum that the government shouldn’t hold back on whatever fiscal support is needed to get businesses and households through this crisis, and with the European Central Bank buying Greek bonds the government can step up borrowing if needed. Nevertheless, the country’s debt levels do mean that this requires the forbearance of the country’s creditor institutions.

That’s an uncomfortable situation for any government to be in. Greece’s is the euro-area’s most extreme case, but it’s not alone. Unlike the US, where the government started writing stimulus cheques early in the crisis, the centre-piece of Europe’s grand fiscal response to the crisis has been the Recovery and Resilience Facility, which won’t start distributing funds until the latter part of this year. Until then national budgets have to fill the gap. This is a big ask, and I suspect the question of fiscal support for national economies will return to the top of the EU agenda sooner rather than later.

For Greece, now, the question is how long the government holds its nerve as the bills mount. As the legendary football manager Alex Ferguson once said, it’s squeaky bum time.

Data summary:

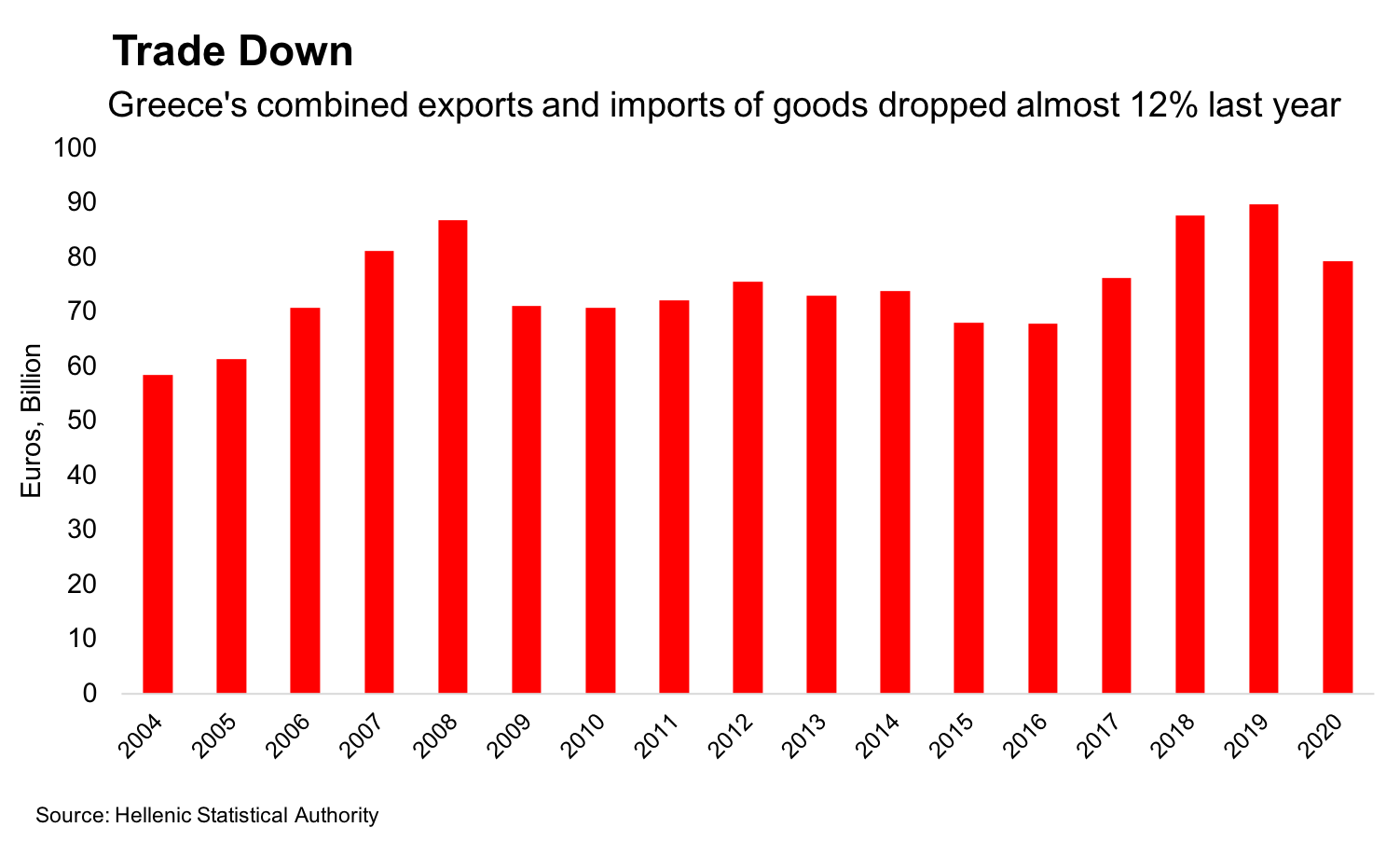

Elstat today released December data on the country’s commercial transactions — export and import of goods — with the month’s trade deficit dropping 10.8 percent compared with December 2019. For the whole of 2020, the trade deficit fell 18.5 percent as imports shrank by more than exports. Total trade last year — imports and exports — dropped 11.6 percent from 2019.

Greece’s manufacturing Purchasing Managers’ Index increased to 50 in January from 46.9, putting it at exactly the level signalling neither expansion nor contraction. Markit noted that firms faced their sharpest rate of cost inflation since July 2008, with a small part of this passed on to customers.

Credit growth addendum

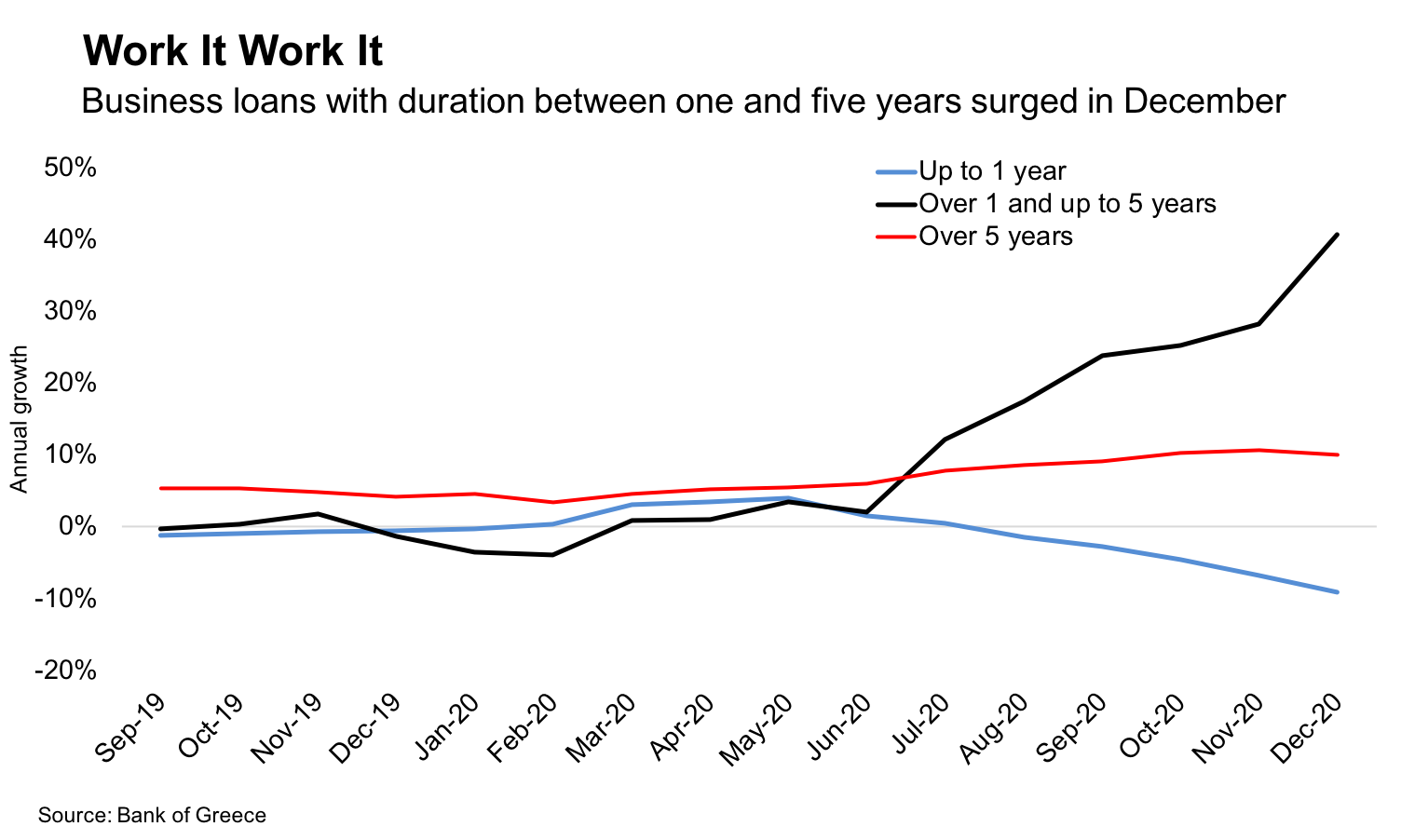

We mentioned the increase in bank lending to the private sector in last week’s roundup, but since the data came out on Friday afternoon I didn’t take a detailed look at the breakdown before the newsletter came out.

Having now done so, the category that most jumped out at me was a surge in business lending with duration between one and five years, a 41 percent annual growth rate in December from 28 percent the month before.

That duration corresponds with two-year working capital loans, with subsidised interest, that the banks were offering small and medium-sized businesses hit by the pandemic under the government’s TEPIX II vehicle.

The Bank of Greece data breaks down the amount of loans to non-financial corporations going to SMEs, and it breaks down the duration of business loans, but unfortunately it doesn’t offer a breakdown of both. So it’s impossible to say from the data how much of this surge corresponded to working capital loans to SMEs.

However, we can see that in the month of December net credit flows to SMEs amounted to 715 million euros from 96 million euros in November. We can also see that the net flow of business loans with duration between one and five years increased 1.18 billion euros, compared with 428 million euros in November.

Loans with a duration of up to one year decreased 191 million euros in December, and have been steadily dropping since April — suggesting that companies have been refinancing existing working capital on more favourable terms.

If you’re enjoying this newsletter, consider sharing it with others who might also like it.

Next week’s key data

Tuesday:

December industrial production (Elstat)

Thursday:

November unemployment (Elstat)

Friday:

November building activity (Elstat)

Elsewhere on the web

Along the same theme as we started this roundup with, Thomas Wieser — he of many a briefing by “an unnamed EU official” during Greece’s debt crisis — also says that Europe must start answering fiscal policy questions. I don’t know whether or not I’d like his proposed answers, but he lays out the right questions

This will be a tough one to break to my daughters if it closes: Nick Paphitis of the Associated Press reports on Attica Zoological Park’s lockdown troubles

The Bank of Greece last month published its twice-yearly Economic Bulletin, which always contains interesting research on the Greek economy

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.