Macro roundup: Record low for housing loans

Lending growth slows; deposit composition shifts; retail sales fall

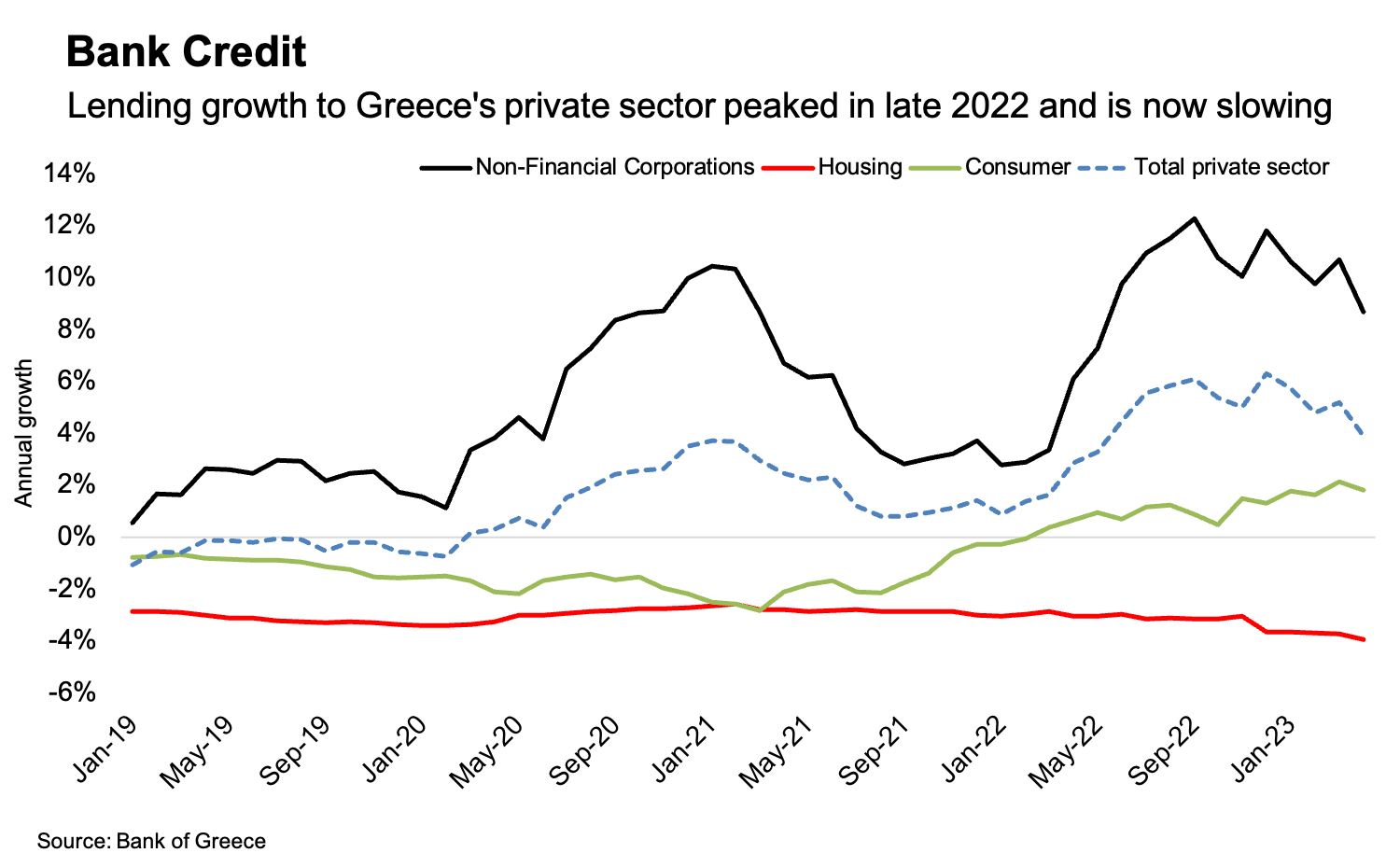

Bank lending to Greece’s private sector continued its downward trajectory in April, as tightening monetary conditions drove already-depressed mortgage lending to its biggest contraction on record.

Private-sector credit grew at an annual rate of 3.9 percent, down from 5.2 percent in March and 4.8 percent in February. In terms of net flows, there was a 789 million-euro reduction in net lending to the private sector in April, following a 1.22 billion-euro increase the month before.

Lending to business grew 8.7 percent in April, down from 10.7 percent the month before. For households, lending fell 2.7 percent compared with 2.5 percent in March.

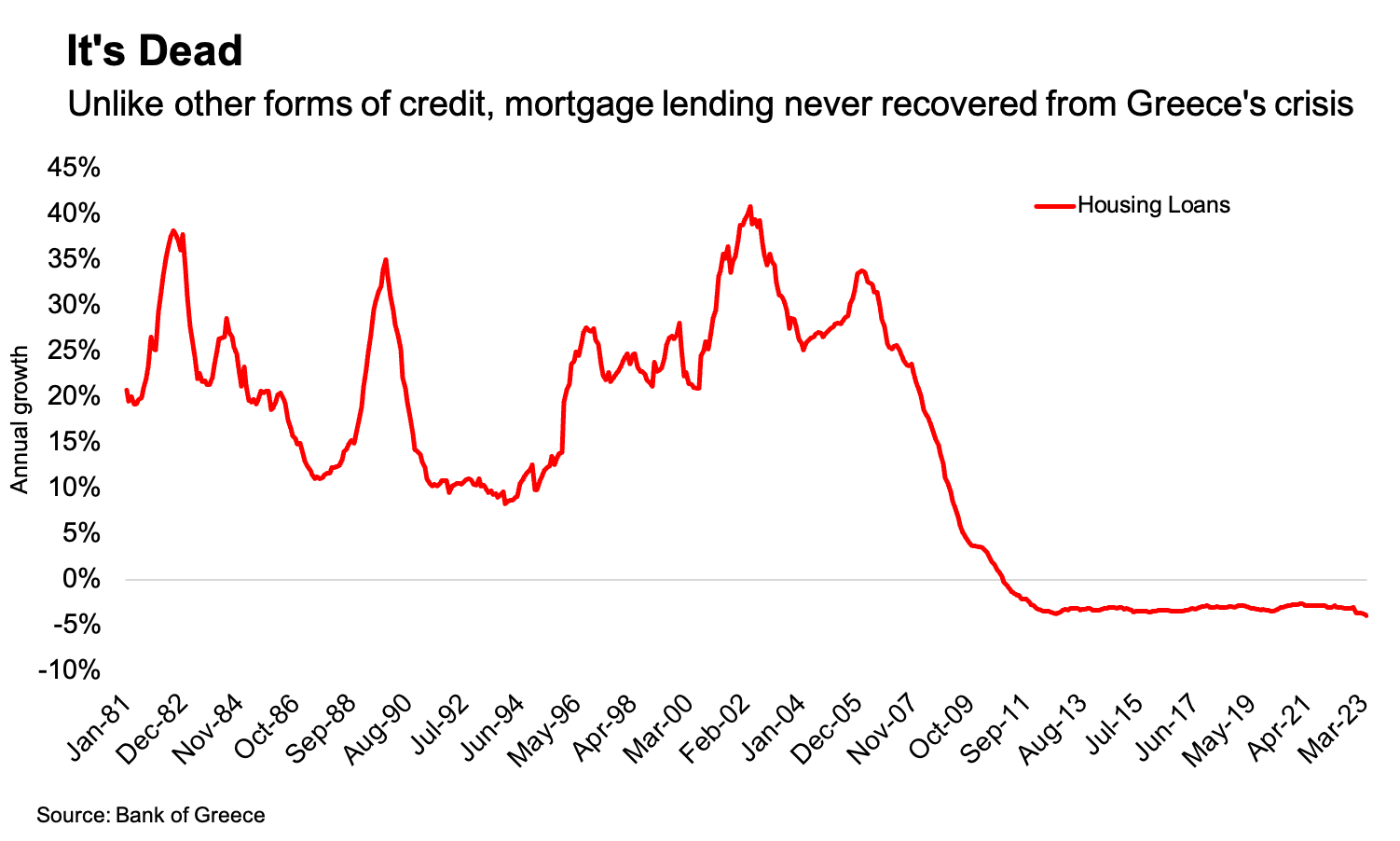

The annual contraction in housing loans reached 4 percent, down from 3.7 percent the month before. Mortgage lending has been at depressed levels since the financial crisis, consistently contracting at a rate of at least 2 percent over a decade. So the latest data point doesn’t represent a sudden drop. Nevertheless, the contraction in April is the largest recorded in Bank of Greece data going back to 1981.

Consumer credit grew 1.7 percent in April, down from 2.1 percent in April. Despite the growth, in absolute numbers this category is small, with net borrowing in the 12 months through April increasing by just 156 million euros. To put that into context, household deposits in this period increased by 5.56 billion euros.

Deposit rotation

Private sector deposits in Greece fell by 15 million euros in April, after increasing 2.32 billion euros the month before. In the first four months of the year, private sector deposits fell by 3.66 billion euros.

Falling business deposits have been chiefly responsible for the overall private sector drop. For households, deposits increased by 1.13 billion euros in April, and by 246 million euros in the first four months of the year.

Aside from the overall flows, a distinct trend that is occurring this year is that Greek households are moving their deposits from overnight accounts to term deposit accounts, which are starting to offer higher interest rates.

Other data

Greece’s unemployment rate crept up to 11.2 percent in April from a revised 11.1 percent in March

Retail sales decreased 0.3 percent in March from a year earlier, while retail volume fell 8.7 percent

Sales fell 0.3 percent in the food sector; 13.7 percent for automotive fuel

Volume fell 11 percent in the food sector and 13.4 percent for supermarkets

Automotive fuel volume fell 6.9 percent

Greece’s manufacturing purchasing managers index dropped to 51.5 in May from 52.4 in April, according to S&P Global

A reading above 50 signals improved operating conditions in the sector

The rate of new order growth “eased to only a marginal pace”, while the pace of expansion in employment also softened, according to S&P Global

“Although mentioning efforts to run down stock levels, firms continued to purchase inputs in response to greater production requirements.”

Economic sentiment in Greece worsened slightly in May, according to the European Commission’s economic sentiment indicator

Consumer confidence improved to -34.5 from -44.6

Sentiment worsened in industry, retail and services

Overall ESI reading was 108.1 in May, down from 108.7 in April

Slowdown coming?

It’s worth taking a moment to briefly note that this week’s releases in the “other data” section are all pointing in the same direction — that the general slowdown in Europe has also starting to affect Greece’s economy.

Two aspects of the data stood out to me in particular. One was the large drop in retail volumes — particularly in the food sector, where inflation is still running in double digits. This indicates that the price elasticity of demand for food is maybe higher than we imagined, as consumers adjust to the rising cost of living.

The other thing that stood out was S&P Global’s passing reference in the PMI report to firms’ efforts to run down stock levels.

An aspect of last year’s strong economic growth that hasn’t been remarked on much is the extent to which changes in inventories were an important driver — contributing 2.4 percentage points to the 5.9 percent increase in gross domestic product. That’s likely to prove a drag on growth this year as inventories adjust — unless the experience of the supply chain bottlenecks of 2021 and early 2022 caused a structural shift whereby firms want to hold more stock. The PMI report that managers want to run down stocks gives us an anecdotal hint that we’re not seeing a structural shift.

Next week’s key releases

Tuesday, June 6:

April interest rates on bank loans and deposits (Bank of Greece)

Wednesday, June 7:

First-quarter gross domestic product (Elstat)

April commercial transactions (Elstat)

Friday, June 9:

May consumer price index (Elstat)

April industrial production (Elstat)