Funding Greek industry

Credit growth last quarter was mostly channeled towards manufacturers and utilities

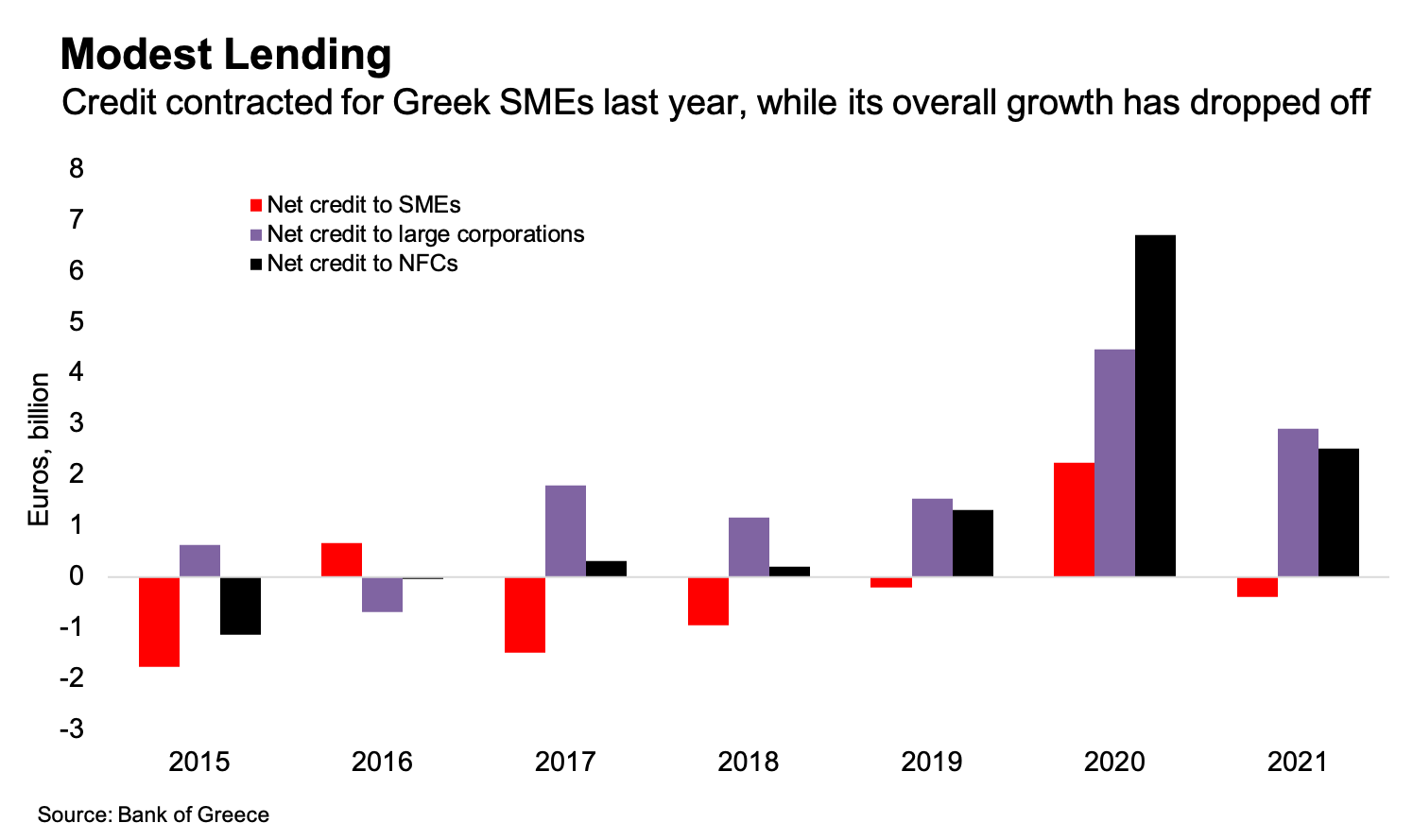

In our last roundup we noted the big drop in lending to small and medium-sized businesses in December. But what made that drop even more noteworthy was that there was a huge increase in lending to businesses overall.

In fact, the 1.5 billion-euro increase in lending to non-financial corporations was the second largest since 2010 — with the biggest coming at the start of the first lockdown in in March 2020, when there was a surge in working capital credit for large corporations. Subtracting lending to SMEs from overall lending to NFCs, net credit flows to large corporations in December amounted to 2.4 billion euros.

As for the general uptick in lending in the last few months of the year, 88 percent of net lending to NFCs happened in the last quarter. So while the credit expansion was disappointing for the year as a whole — net flows to NFCs amounted to 2.5 billion euros, a 63 percent drop from 2020, while flows to SMEs were negative — hopefully the strong finish to the year might be a sign of some momentum building.

Especially if the increase in lending is being directed toward greater investment.

If we consider credit to be the primary channel through which capital allocation takes place in an economy, it’s interesting to take a look at which economic sectors bank lending is flowing to.

The Bank of Greece’s sectoral breakdown for all non-financial corporations — so including SMEs — shows that lending in the fourth quarter was heavily directed towards Greek industry, split fairly equally between “manufacturing, mining and quarrying” and “electricity, gas and water supply”. The latter category accounted for more of December’s lending, with 458 million euros of net flows, while there were also 275 million euros of flows to real estate in that month.

It would be stretching things too far to look at a few months-worth of lending to industry and conclude that this is a harbinger of greater investment in Greece’s economic capacity.

However, already before the fourth quarter there were encouraging signs in the national accounts data of investment creeping up, and hopefully this will be further accelerated by projects with European Union funding from the Recovery and Resilience Facility.

I’d love to get your thoughts and feedback, either in the comments, on Twitter or by reply if you received the newsletter by email. If you’re not subscribed yet, consider doing so now.